Dividend taxation in the EU looks straightforward until investors receive their first foreign dividend payment. A €100 dividend paid by a French company to a German investor may lose tax before it even reaches the broker account — and then face additional taxation again in Germany. That is why two investors holding the same stock can end up with very different after-tax returns.

The problem is that dividend taxation in the EU rarely stops at one layer. First, the country paying the dividend may automatically withhold part of the income. Then the investor’s country of tax residence may tax the same dividend again, while tax treaties and foreign tax credits determine how much can realistically be offset or reclaimed.

ETFs make the picture even less transparent. An Irish ETF holding US dividend stocks can create a completely different tax outcome from directly owning local shares, even when the investor sees only one payment arriving in their account. In practice, the headline dividend tax rate tells investors surprisingly little. Broker handling, treaty access, reclaim procedures and ETF structure can have just as much impact on the final after-tax yield.

Across the EU, the investors who keep more of their dividend income are usually not the ones chasing the highest yields — but the ones using lower-friction tax structures.

Disclaimer

This article is for informational and educational purposes only. It explains how European tax systems are generally structured and does not constitute tax, legal, or financial advice. Tax rules vary widely across countries and depend on individual circumstances, including income sources, employment status, residence, and recent legislative changes. The examples and references used are simplified and illustrative, not personalized. For decisions involving specific tax situations, local regulations and qualified professionals should always be consulted.

What Actually Matters Most for EU Dividend Investors?

For most investors, dividend taxation in the EU is less about finding the “lowest tax country” and more about understanding how much of each dividend payment is lost before the money reaches their account.

| Investor Goal | What Usually Matters Most |

|---|---|

| Keeping more dividend income | Reducing foreign withholding tax and using efficient treaty structures |

| Avoiding paperwork | Fast reclaim systems and strong broker support |

| ETF investing | Fund domicile and internal withholding efficiency |

| Living abroad | Tax residence and local reporting obligations |

| Building passive income | After-tax yield, not headline dividend yield |

The headline withholding rate rarely tells the full story. A country with slightly higher taxes but efficient treaty relief can produce a better investor experience than a lower-withholding system with slow reclaim procedures, extra documentation and poor broker integration.

That is one reason many EU investors increasingly focus on simplicity and tax friction rather than tax rates alone. In practice, the systems that feel most investor-friendly are usually the ones where withholding, reporting and reclaim processes work smoothly across borders.

Why Dividend Taxation Feels So Complicated in the EU

Dividend taxation across the EU often feels far more confusing than investors expect. The main reason is simple: in many cases, you are not dealing with just one tax system. A single dividend payment can pass through several different layers of taxation before the money finally lands in an investor’s account — especially when the shares, ETFs and tax residency all sit in different countries.

The confusion is not only about different tax rates between EU member states. Some countries deduct tax immediately through withholding tax before the investor even sees the payment. Others place more emphasis on taxing investment income afterwards through domestic tax rules. Then there are tax treaties, broker procedures, custody chains and ETF structures sitting somewhere in between, quietly complicating the process even further.

For investors, the result is often a frustrating disconnect between the “official” dividend tax rate and the amount of money they actually keep. Two countries can appear fairly similar on paper while producing noticeably different after-tax outcomes in reality.

Things usually start to make more sense once investors understand the difference between source-country taxation and residence-country taxation.

A Dividend Can Be Taxed in Two Different Countries

One of the most common misunderstandings around EU dividend taxation is the belief that investors only pay tax in the country where the company is based. In practice, cross-border dividends often involve two separate tax systems at the same time.

Take a simple example: a company in France pays a dividend to an investor who lives and pays taxes in Germany.

France is considered the “source country” because that is where the dividend originates. Germany, meanwhile, is the investor’s “country of tax residence” because the investor is taxed there on worldwide income.

In real-world investing, France may withhold part of the dividend before the payment even reaches the investor’s brokerage account. Germany may then tax that same dividend again under German investment income rules, although foreign tax credits can sometimes reduce part of the overlap.

This is exactly why many investors feel as though they are being taxed twice. Tax treaties are designed to reduce or prevent double taxation, but from the investor’s side the process rarely feels straightforward — especially once reclaim forms, tax certificates and broker reporting requirements start appearing.

And that leads to another major source of confusion: withholding tax is not always the investor’s final tax bill.

Withholding Tax Is Not Always Your Final Tax Bill

A lot of investors assume that the tax deducted automatically by their broker is the full amount they owe. In reality, withholding tax is often only the first layer.

When a foreign company pays a dividend, part of that payment may be withheld before the money reaches the investor at all. The broker simply receives the reduced amount and credits it to the account. On many international brokerage platforms, the entire process happens quietly in the background, with investors barely noticing how much depends on the broker, the custody chain and the account structure being used.

But the investor’s home country may still tax the dividend afterwards. A German resident receiving dividends from France, for example, may still need to declare that income again in Germany even after French withholding tax has already been deducted.

This is where foreign tax credits start becoming important. Many EU countries allow investors to offset at least part of the foreign tax already paid abroad. In theory, that helps reduce the risk of full double taxation. In practice, however, the final outcome depends on treaty rules, domestic tax systems and whether reduced treaty withholding rates were correctly applied somewhere along the brokerage and custody chain in the first place.

The reclaim process itself can also become surprisingly bureaucratic. In some cases, investors may need tax residency certificates, local forms or direct refund applications just to recover excess withholding tax from another country’s tax authority.

That administrative friction is one reason many dividend investors eventually begin prioritising simplicity alongside yield and tax efficiency.

Why Two Investors Can Receive Different Net Dividends From the Same Stock

Two investors can own exactly the same shares and still end up receiving very different net dividend income after tax. Usually, the difference comes down to structure rather than the stock itself.

The first major factor is tax residence. An investor living in Portugal may face a very different outcome from an investor living in Poland, even if both hold the same French dividend stock. Local tax rules, treaty access and reporting obligations all shape the final result.

Broker handling also matters more than many investors realise. Some brokers and custody chains automatically apply treaty-reduced withholding rates whenever possible, while others default to the maximum withholding rate unless additional paperwork has already been completed in advance. Two investors holding the same US dividend ETF through different brokers may therefore receive noticeably different after-tax payments.

ETF structure adds yet another layer of complexity. An Irish-domiciled UCITS ETF holding US dividend stocks can produce a different withholding outcome from directly owning the same shares through a brokerage account. In some situations, part of the tax friction exists inside the ETF structure itself rather than appearing clearly on the investor’s statement.

Even local reporting systems can significantly change the investor experience. Countries such as Denmark and France often involve more administrative reclaim procedures for foreign investors than systems built around flatter taxation models or simpler reporting rules.

For long-term investors, this is why headline dividend yield often matters less than after-tax efficiency. Understanding how multiple tax systems interact across borders is usually far more valuable than simply chasing the highest-paying dividend stocks.

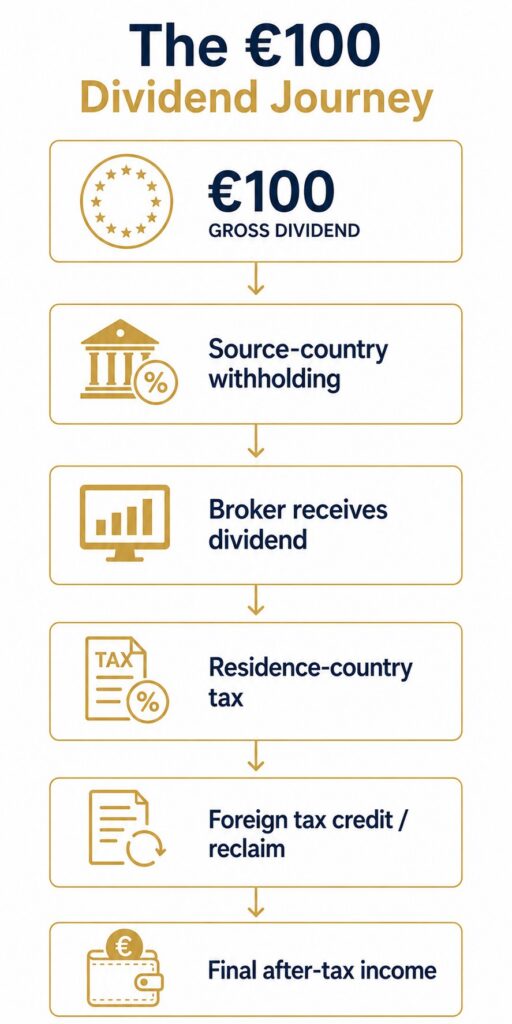

The €100 Dividend Journey

One reason dividend taxation feels so opaque to many EU investors is that the process almost never happens in a single step. By the time a dividend reaches the investor’s account, it may already have passed through several different layers of taxation, withholding procedures and reporting systems.

A simplified €100 dividend journey often looks something like this:

| Stage | What Happens | Example |

|---|---|---|

| Gross dividend | Company declares payment | €100 |

| Withholding tax | Source country deducts tax | Reduced amount after source-country withholding |

| Broker credit | Investor receives payment | Reduced amount |

| Residence-country taxation | Local dividend tax may still apply | Additional tax possible |

| Tax credit or reclaim | Foreign withholding partially offset | Partial recovery |

| Final net dividend | Investor’s after-tax income | Varies |

The key point is that most investors never experience dividend taxation as one simple percentage. The final result depends on several moving parts at once: where the company is based, where the investor is tax resident, whether treaty relief is correctly applied and whether the investment is held directly or through an ETF structure.

Over long periods, even relatively small layers of tax friction can compound. For income-focused portfolios especially, the gap between a low-friction structure and a high-friction one can become much more significant than many investors initially expect.

Scenario 1 — Domestic Investor

The simplest dividend setup is usually a domestic investor holding domestic shares.

Imagine an investor living in Germany who owns shares in a German company through a local brokerage account. The dividend is paid domestically, and withholding is generally handled automatically within the German investment tax system.

The investor may still need to consider annual allowances, reporting obligations or investment-income thresholds depending on the account type and total income level. But compared with cross-border investing, the overall process tends to feel relatively straightforward because the investment interacts primarily with a single tax framework.

That is one reason domestic dividend investing usually creates far less administrative friction than international investing within the EU.

Scenario 2 — Cross-Border EU Investor

Now consider a far more common modern investing situation: an investor living in Germany owns shares in a French company.

The dividend originates in France, where withholding tax may be deducted before the payment even leaves the country. The broker then receives the reduced amount and credits it to the investor’s account.

But the process does not necessarily end there. Germany may still tax the dividend under local investment income rules, while foreign tax credits or treaty mechanisms attempt to reduce part of the overlap between the two systems.

This is where practical friction starts becoming very noticeable. Some investors may need additional documentation to reclaim excess withholding tax or confirm treaty eligibility. Processing times can stretch for months, particularly when several intermediaries sit between the company paying the dividend and the final investor.

In practice, many investors eventually discover that the administrative burden matters almost as much as the tax rate itself.

Scenario 3 — EU Investor Holding US Stocks

US dividend stocks add another layer of complexity for EU investors because the investment sits outside the EU tax framework while still interacting with local residence-country taxation rules.

A European investor holding US shares will usually encounter US withholding tax first. For many international investors, the default withholding rate can be reduced if the correct tax documentation — most commonly the W-8BEN form — has been submitted through the broker beforehand.

The form itself is relatively simple, but many investors only realise how important it is after noticing a much larger-than-expected reduction in their dividend payments.

ETF structure matters here as well. An Irish-domiciled UCITS ETF holding US dividend stocks can produce a different withholding outcome from directly owning the same US shares through a standard brokerage account. This is one reason Irish-domiciled UCITS ETFs became so widely used among European investors over the past decade.

For long-term investors building international portfolios, the interaction between US withholding rules, ETF domicile and local residence-country taxation can have a meaningful effect on after-tax returns over time.

The next step is understanding how different EU tax systems approach dividend income — and why some systems feel noticeably easier for international investors to navigate than others.

4 Common Dividend Tax Environments Investors Encounter Across the EU

One reason dividend taxation feels so difficult to compare across the EU is that there is no single “European” model. Different countries approach dividend taxation in very different ways. Some rely heavily on withholding tax at source, while others focus more on standardised investment-income taxation, treaty efficiency or administrative simplicity for investors.

And for investors, the practical experience often matters just as much as the official tax rate itself. Two countries may publish fairly similar dividend tax rates on paper while creating completely different levels of paperwork, reclaim complexity or ETF efficiency once cross-border investing enters the equation.

That is why it usually makes more sense to think of Europe not as one unified dividend-tax area, but as a collection of different tax environments that investors regularly encounter in practice.

High-Withholding Systems

Countries such as France and Denmark are often associated with higher-withholding environments for international investors.

The difficulty is not only the withholding rate itself. In many cases, the bigger issue is the reclaim process. Recovering excess tax withheld above treaty limits can become slow, administrative and frustrating once foreign investors start dealing with local tax procedures.

In practice, investors may need:

- tax residency certificates

- additional broker documentation

- local refund forms

- lengthy processing periods

For long-term dividend investors, this can create meaningful friction even when treaty relief technically exists on paper.

That does not necessarily make these systems unattractive. France and Denmark both remain important equity markets with significant international investor participation. But compared with systems built around simpler investment-income taxation or lower-withholding structures, the overall administrative experience can feel noticeably heavier.

Structured Investment-Tax Systems

Countries such as Germany, Italy and Poland are often viewed as more structured investment-tax systems built around relatively standardised taxation frameworks.

For investors, the main advantage is usually predictability. Dividend income is often integrated into broader investment-income taxation systems rather than depending heavily on fragmented local rules, reclaim-heavy processes or overlapping tax treatments.

That does not mean these countries are necessarily low-tax. Germany, for example, can still feel relatively substantial from a dividend-tax perspective once solidarity surcharges and related investment-tax rules are included. But many investors find the structure itself easier to follow than systems where reclaim procedures dominate the experience.

For domestic investors especially, these systems often feel administratively cleaner because withholding, reporting and investment-income treatment are usually more integrated.

Cross-border investing can still create complications, of course. But the underlying framework tends to feel more standardised and easier to navigate from the investor’s perspective.

Comparatively Lower-Friction Systems

Countries such as Greece, Croatia and Romania are sometimes perceived as comparatively simpler from an administrative perspective in certain investment situations.

Part of that perception comes from lower-withholding structures in some cases. But simplicity itself also matters. Investors tend to value systems where reporting obligations, reclaim procedures and investment-tax rules feel easier to understand and manage in practice.

That does not automatically make these countries “tax havens” for dividend investing. Residence-country taxation, treaty access and broader personal tax rules still play a major role in determining the final outcome.

Still, for smaller investors especially, reclaim paperwork can sometimes outweigh the value of the refund itself. Systems that create less administrative friction can therefore become surprisingly attractive for investors managing smaller international portfolios.

This is one reason internationally mobile investors increasingly pay attention not only to headline tax rates, but also to usability and administrative efficiency.

International Investment Hubs

Countries such as Ireland, the Netherlands and Portugal play a slightly different role within the European investment landscape.

These systems matter not only because of domestic dividend taxation, but also because of their importance to international investment structures, ETF ecosystems and treaty networks.

Ireland in particular became central to the European UCITS ETF market, partly because Irish fund structures interact relatively efficiently with international withholding-tax systems in many common investment scenarios. The Netherlands also plays an important role in cross-border investment structuring and capital flows within Europe.

Portugal attracts attention for a different reason. For many internationally mobile investors, the country sits at the intersection of tax residency planning, international lifestyle migration and investment structuring.

For many investors, these countries matter less as straightforward “low-tax” destinations and more as infrastructure hubs within the broader European investment system.

The next step is comparing how these systems differ in practice — not just through headline tax rates, but through reclaim difficulty, investor complexity and overall tax friction.

EU Dividend Tax Comparison Table

Dividend taxation across the EU is difficult to reduce to a simple ranking because investors are rarely comparing tax rates alone. Administrative complexity, treaty access, ETF structures and reclaim procedures can all have a meaningful impact on the real investor experience.

The table below is intended as an editorial comparison rather than a precise tax-scoring system. It reflects broad investor-facing patterns that are commonly discussed in cross-border European investing.

| Country | Typical Dividend WHT Environment | Investor Complexity | Treaty Efficiency | ETF Relevance | Overall Friction |

|---|---|---|---|---|---|

| France | High | High | Medium | Medium | High |

| Denmark | High | High | Medium | Low | High |

| Germany | Medium | Medium | High | High | Medium |

| Italy | Medium | Medium | Medium | Medium | Medium |

| Poland | Medium | Medium | Medium | Low | Medium |

| Greece | Low–Medium | Low–Medium | Medium | Low | Low–Medium |

| Croatia | Low–Medium | Low | Medium | Low | Low–Medium |

| Romania | Low | Low | Medium | Low | Low |

| Ireland | Medium | Low–Medium | High | High | Low–Medium |

| Netherlands | Medium | Medium | High | High | Medium |

| Portugal | Medium | Medium | Medium | Medium | Medium |

These categories are intentionally broad. Actual investor outcomes still depend heavily on tax residence, treaty eligibility, broker structure, ETF domicile and local reporting obligations. A country with relatively low withholding tax can still create substantial paperwork, while a higher-tax system may feel easier to manage if treaty access and reclaim procedures function efficiently.

For many international investors today, ETF structure increasingly matters just as much as the domestic dividend-tax system itself.

How ETFs Change Dividend Taxation

ETFs changed the way many Europeans invest internationally, but they also made dividend taxation significantly harder to understand.

A domestic investor buying local shares can usually see where dividends are paid and where tax is deducted. ETF structures introduce additional layers between the investor and the underlying assets. That changes how withholding tax is applied, how dividend income moves across borders and how much of the tax friction remains visible to the end investor.

For many retail investors, the confusion begins when the ETF and the underlying shares are based in different countries.

Distributing vs Accumulating ETFs

One of the most common misunderstandings in European investing is the belief that accumulating ETFs completely avoid dividend taxation.

In reality, the difference is mostly about how income is handled inside the fund structure itself.

A distributing ETF pays dividend income directly to investors. An accumulating ETF, meanwhile, reinvests that income back into the fund instead of sending cash payments to the investor’s account.

From the investor’s perspective, accumulating ETFs can feel simpler because there are fewer visible dividend payments. But that does not mean withholding taxes disappear at the fund level, and local tax treatment still depends heavily on the investor’s country of residence.

This distinction matters because many investors focus only on the visible dividend payment while overlooking the tax treatment happening quietly inside the ETF structure itself.

Why Irish ETFs Became So Popular With European Investors

Ireland became one of the most important ETF domiciles in Europe partly because Irish UCITS fund structures interact relatively efficiently with US withholding-tax systems in many common investment situations.

That became especially relevant for European investors buying:

- S&P 500 ETFs

- global equity ETFs

- US dividend-focused funds

For many international investors, Irish-domiciled ETFs offered a combination of:

- broad UCITS compatibility

- access through major European brokers

- strong cross-border fund recognition

- relatively efficient interaction with US withholding-tax rules

That does not mean Irish ETFs are universally more efficient in every situation. Local residence-country taxation still matters, and ETF taxation remains highly dependent on the investor’s own circumstances.

But for many Europeans building international portfolios through platforms such as Interactive Brokers, Trade Republic or DEGIRO, Irish UCITS ETFs gradually became the default structure for global investing.

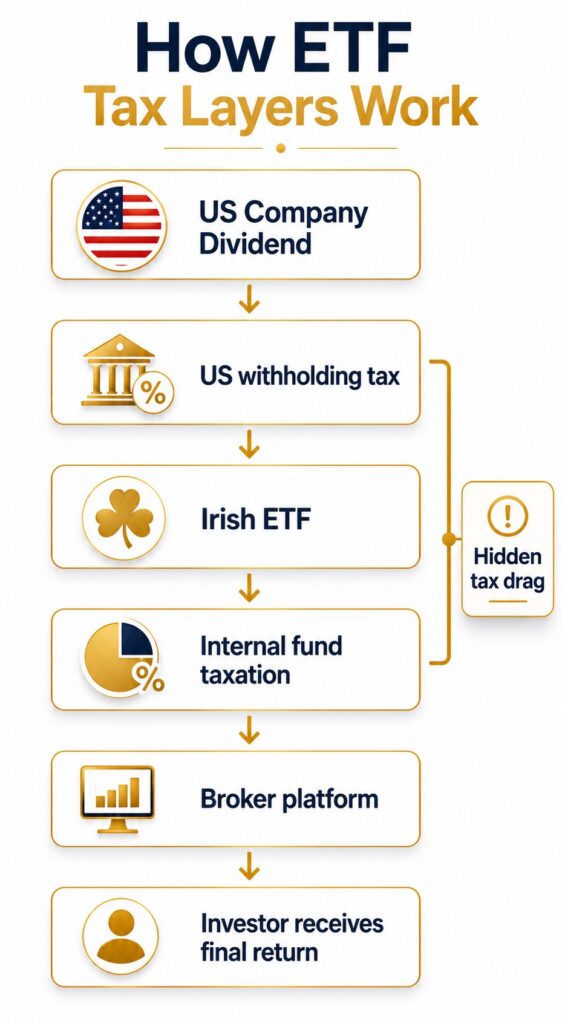

The Hidden Tax Layer Inside Some ETFs

One of the least understood aspects of dividend taxation is that some withholding taxes can exist entirely inside the ETF structure itself.

An investor may see a headline ETF return without realising that part of the underlying dividend income was already reduced before it ever reached the fund.

This is often described as internal withholding-tax drag. The investor does not necessarily see the deduction directly on the brokerage statement because the tax friction occurs between:

- the underlying company

- the source-country tax authority

- the ETF structure

- the fund custodian

As a result, two ETFs tracking very similar indexes can still produce slightly different long-term outcomes depending on:

- fund domicile

- treaty access

- custody structure

- internal withholding efficiency

Many retail investors misunderstand this because they focus mainly on ETF fees or visible dividend yield. In reality, invisible withholding friction inside the structure can matter just as much over long investment horizons.

For international investors, understanding ETF taxation increasingly means understanding the layers beneath the visible portfolio itself.

The next step is examining how tax treaties attempt to reduce this cross-border friction — and why reclaiming foreign withholding tax can still become surprisingly complicated.

How Tax Treaties Actually Reduce Dividend Tax

Tax treaties are one of the main reasons cross-border dividend investing inside the EU remains manageable at all. Without them, investors could face far more overlap between tax systems every time dividend income moves from one country to another.

In practice, though, tax treaties rarely remove complexity completely. What they usually do is reduce withholding-tax rates, define how taxing rights are shared between countries and create mechanisms that help investors offset part of the foreign tax already paid abroad.

For investors, that distinction matters. Treaties often reduce friction, but they do not automatically eliminate paperwork, delays or reporting obligations.

Why Investors Think They Are Being Taxed Twice

Many investors feel they are being taxed twice because they see money deducted before the dividend reaches their account and may still need to declare the same income again in their country of residence.

A typical example involves a resident of Germany receiving dividends from a company based in France.

France may apply withholding tax at source before the payment leaves the country. Germany may then include the dividend within German investment-income taxation rules because German residents are generally taxed on worldwide investment income.

From the investor’s perspective, the same dividend can appear to be taxed twice.

In reality, tax treaties and foreign tax-credit systems are designed to reduce or mitigate that overlap. But the process does not always feel seamless because withholding happens first, while credits, offsets or reclaim procedures may happen later through tax reporting or refund applications.

This timing difference is one reason cross-border dividend taxation often feels more punitive than it technically is.

What Tax Treaties Really Change

For investors, tax treaties mainly affect three areas:

- withholding-tax rates

- foreign tax credits

- reclaim procedures

The first effect is usually the most visible. Many treaties reduce the maximum withholding tax one country can apply to investors who are resident in another treaty country.

But reduced treaty rates are not always applied automatically. In some situations, investors need to submit residency documentation or additional tax forms before the lower treaty rate becomes available.

Tax treaties also help determine whether taxes already paid abroad can be credited against local investment-income taxation. This is why many investors encounter terms such as “foreign tax credit relief” during annual tax reporting.

The third area is reclaim procedures. If withholding tax was deducted above treaty limits, investors may be able to apply for a refund from the foreign tax authority.

In theory, this creates a more balanced cross-border system. In reality, the process can become surprisingly administrative depending on:

- the countries involved

- the broker structure

- local tax-authority procedures

- document requirements

- processing times

For many retail investors, the challenge is not understanding that treaties exist. It is understanding how to access the benefits efficiently in practice.

Why Reclaiming Dividend Tax Can Be Frustrating

Foreign withholding-tax reclaims are easily one of the least investor-friendly parts of international dividend investing.

The process can involve:

- tax residency certificates

- treaty eligibility forms

- broker confirmations

- translated documents

- paper-based administration

- long waiting periods

Some countries require investors to obtain official residency certification from their domestic tax authority before a reclaim request can even be filed. Others require separate forms for every dividend-paying country or each individual tax year involved.

Broker limitations can add another layer of friction. Some brokers assist with treaty-rate applications or reclaim services, while others leave the entire process to the investor.

Timing is another major issue. Reclaim procedures can take months and, in some cases, considerably longer depending on the tax authority and the documentation involved.

For smaller portfolios especially, investors sometimes discover that the administrative burden outweighs the refund itself. That is one reason many international investors increasingly focus on structures that minimise withholding friction from the beginning rather than relying heavily on reclaim procedures afterwards.

In practice, the most tax-efficient structure is not always the one with the lowest headline tax rate — but the one investors can realistically manage without excessive administrative complexity.

Dividend Taxes for Expats and Cross-Border EU Investors

Dividend taxation becomes noticeably more complicated once investors start living, working or investing across multiple countries.

For many expats, the difficulty is not simply the tax rate itself. The bigger challenge is understanding which country actually has the right to tax the dividend income, how treaty rules apply and whether local reporting obligations still exist even after withholding tax has already been deducted abroad.

That is one reason many cross-border investors eventually realise that international dividend taxation is less about finding the “lowest-tax country” and more about understanding how several tax systems interact at the same time.

Your Tax Residence Usually Matters More Than Your Citizenship

One of the most common misunderstandings among EU investors is the assumption that citizenship determines how international dividends are taxed.

In most cases, tax residence matters far more.

An Italian citizen living and paying taxes in Portugal may be treated very differently from an Italian citizen who remains tax resident in Italy. The exact same dividend portfolio can therefore produce different reporting obligations, treaty outcomes and after-tax income depending on where the investor is considered tax resident.

This becomes especially important for internationally mobile professionals, remote workers and retirees living across multiple jurisdictions.

Tax-residency rules themselves can quickly become technical. Different countries use different tests involving:

- physical presence

- permanent-home location

- centre-of-life factors

- economic ties

- domestic residency rules

- treaty tie-breaker provisions

For investors, though, the practical takeaway is fairly simple: moving countries does not automatically change tax treatment unless tax residency itself changes as well.

Common Expat Mistakes

One of the most common mistakes expats make is assuming that withholding tax deducted abroad is automatically the final tax owed.

In reality, many countries still require residents to report worldwide investment income and foreign assets even when foreign tax has already been withheld at source.

Another frequent issue is misunderstanding local reporting obligations. Some investors assume that using an international broker removes local filing requirements. In practice, many countries still require disclosure of:

- foreign brokerage accounts

- overseas dividend income

- ETF holdings

- foreign-source investment income

Residency misunderstandings can create even larger problems. Investors sometimes assume that spending part of the year abroad automatically changes their tax status, while domestic residency rules and treaty frameworks may still classify them as tax resident in their original country.

Cross-border investing also creates timing issues. Tax may be withheld in one country during the year while credits, offsets or reporting adjustments only appear much later through annual tax filings.

For many expats, the complexity does not come from one specific tax rule — but from several systems interacting simultaneously.

Why Moving Countries Does Not Automatically Reduce Dividend Tax

Many investors assume that relocating to a lower-tax country will automatically improve the tax efficiency of their dividend portfolio. In practice, the outcome is usually far more nuanced.

First, source-country withholding taxes often continue to apply regardless of where the investor moves. A French dividend paid to an investor living abroad, for example, may still be subject to French withholding-tax rules before the payment even leaves France.

Second, changing tax residence is rarely immediate or automatic. Some countries apply detailed residency tests, ongoing reporting obligations or relocation-related tax rules that can continue affecting investors long after relocation.

Third, local investment taxation is only one piece of the puzzle. Investors still need to think about:

- treaty access

- ETF domicile

- broker structure

- reporting obligations

- foreign-asset disclosure rules

- reclaim procedures

In some situations, investors discover that lower headline tax rates are partly offset by higher administrative complexity or weaker treaty efficiency.

That is one reason internationally mobile investors increasingly focus on overall tax friction rather than simply searching for the country with the lowest published dividend-tax rate.

For long-term investors, the most sustainable structure is often the one that remains manageable across several tax systems over time — not necessarily the one with the lowest theoretical rate on paper.

The next step is examining which EU systems tend to create the least friction for investors in practice.

Which EU Systems Create the Least Friction for Investors?

For many investors, the most attractive dividend-tax system is not necessarily the one with the lowest headline rate. In practice, usability often matters just as much as taxation itself.

A country with moderate tax rates but straightforward reporting rules, efficient treaty access and manageable reclaim procedures can feel far easier to navigate than a lower-tax system built around heavy paperwork and slow administrative processes.

This becomes especially important for long-term investors managing international portfolios across multiple brokers, ETFs and cross-border investment accounts.

Lower-Friction Systems

Some EU systems are often viewed as easier to navigate from an administrative perspective, particularly for domestic investors or investors with relatively simple portfolio structures.

Countries such as Ireland, Croatia and, in some situations, Romania or Greece are frequently mentioned in this context.

The reasons vary, but often include:

- simpler reporting frameworks

- lower-withholding environments in certain cases

- more standardised investment-income treatment

- ess burdensome reclaim procedures in some situations for some investors

For smaller retail portfolios especially, administrative simplicity can become surprisingly valuable. Many investors eventually realise that reclaim forms, residency certificates and ongoing documentation requirements create more friction than the headline tax rate itself.

That does not mean these systems are universally simpler for everyone. Cross-border holdings, foreign ETFs and international brokerage structures can still introduce significant complexity.

But from a practical standpoint, investors often prefer systems where the overall process feels manageable without constant administrative effort.

High-Paperwork Systems

Other systems are commonly viewed as much heavier from a documentation perspective.

Countries such as France and Denmark are frequently associated with more demanding reclaim procedures, especially when foreign investors try to recover withholding tax deducted above treaty levels.

In some situations, investors may need:

- residency certification

- broker confirmations

- country-specific tax forms

- translated documentation

- repeated submissions across multiple tax years

Processing timelines can also become lengthy depending on the tax authority and the custody chain involved.

For large institutional investors, this may simply be treated as part of international portfolio administration. For smaller retail investors, however, the process can feel disproportionately complicated relative to the value of the refund itself.

That is one reason some investors increasingly prioritise structures that minimise withholding friction upfront rather than relying heavily on reclaim procedures afterwards.

Systems That Work Better for ETF Investors

ETF investors often evaluate dividend-tax systems differently from direct stock investors.

For many Europeans, the main question is not simply domestic dividend taxation, but how efficiently the overall system interacts with:

- UCITS ETF structures

- cross-border withholding frameworks

- international brokers

- US equity exposure

This is one reason Ireland became so central to the European ETF ecosystem. Irish-domiciled UCITS funds are widely used across Europe partly because they interact relatively efficiently with US dividend-withholding systems in many common investment scenarios.

The Netherlands also plays an important role in cross-border fund structures and institutional capital flows within Europe.

For ETF investors, the most efficient system is often not the one with the lowest visible dividend-tax rate. In practice, efficiency usually depends more on:

- fund domicile

- treaty access

- internal withholding treatment

- broker integration

- long-term administrative simplicity

That is why two investors with almost identical ETF portfolios can still end up with different after-tax outcomes depending on how their investment structures are organised across jurisdictions.

In practice, many experienced international investors increasingly optimise for simplicity, predictability and operational efficiency rather than chasing the lowest theoretical tax rate available on paper.

The final step is understanding the mistakes investors most commonly make when trying to optimise dividend taxation across borders.

Common Dividend Tax Mistakes EU Investors Make

Many dividend-tax mistakes are not caused by especially complicated laws. More often, they happen because investors focus heavily on visible dividend yields while underestimating how tax structures shape the final return.

A portfolio that looks highly efficient before tax can become far less attractive once withholding layers, ETF structure, reclaim friction and local reporting obligations enter the picture.

For long-term investors, even relatively small inefficiencies can compound meaningfully over time — particularly in portfolios designed around recurring dividend income.

Chasing Yield Before Tax

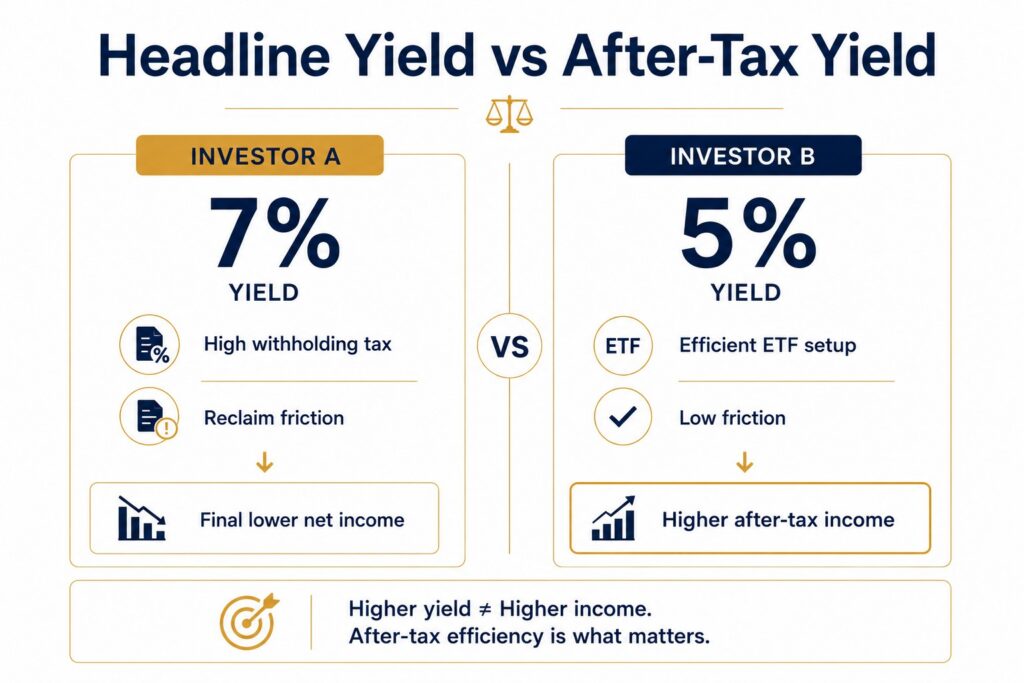

One of the most common mistakes dividend investors make is focusing on headline yield without thinking enough about after-tax income.

A stock showing a visibly higher dividend yield may still produce weaker long-term net returns if:

- withholding taxes are high

- reclaim procedures are inefficient

- foreign tax credits are limited

- additional reporting complexity applies

This becomes especially important in cross-border investing. A dividend that looks attractive on a stock screener or brokerage dashboard can produce a very different result once international withholding rules and residence-country taxation are taken into account.

For many experienced investors, after-tax yield eventually matters far more than the published dividend yield itself.

Ignoring ETF Structure

Many investors spend a great deal of time comparing ETF fees while paying far less attention to the tax structure underneath the fund itself.

ETF domicile, treaty access and internal withholding treatment can all materially affect long-term returns, even when two funds track almost identical indexes.

This is one reason Irish-domiciled UCITS ETFs became so widely used among European investors seeking US equity exposure and global index diversification.

The issue is not simply taxation at the investor level. In many cases, part of the tax friction occurs quietly inside the ETF structure before the investor even sees the final return or dividend distribution.

As a result, two ETFs tracking nearly identical indexes can still produce slightly different long-term outcomes depending on:

- fund domicile

- withholding efficiency

- custody structure

- cross-border treaty interaction

For international investors, understanding ETF taxation increasingly means understanding what happens beneath the surface of the investment structure itself.

Assuming Broker Withholding Is Final

Another common misunderstanding is assuming the tax withheld by the broker automatically represents the investor’s final tax obligation.

In reality, withholding tax is often only the first stage of the process.

The investor’s country of tax residence may still require:

- local reporting

- declaration of worldwide investment income

- foreign-asset disclosure

- additional investment-income taxation

At the same time, some investors may also qualify for foreign tax credits or withholding-tax reclaims depending on treaty rules and local tax systems.

This creates a situation where the amount visible on the brokerage statement does not always reflect the investor’s final after-tax position.

For expats and internationally mobile investors especially, the gap between broker withholding and actual tax liability can become very important.

Focusing Only on Headline Tax Rates

Headline dividend-tax rates can be surprisingly misleading when viewed in isolation.

Two countries with very similar published tax rates can still produce completely different investor experiences depending on:

- reclaim efficiency

- treaty access

- ETF interaction

- broker infrastructure

- reporting obligations

- administrative complexity

A system with a slightly higher headline tax rate may still feel easier — and sometimes more efficient — to navigate if withholding relief works smoothly and ongoing compliance remains manageable.

That is one reason many experienced international investors focus less on finding the “lowest-tax country” and more on reducing long-term tax friction across the entire investment structure.

In practice, simplicity, predictability and operational efficiency often matter more than theoretical optimisation alone.

Ultimately, the real challenge is not simply understanding dividend taxation across Europe — but building investment structures that remain manageable across borders over time.

Dividend Tax Friction Score (Finorum Editorial Framework)

Headline dividend-tax rates rarely tell investors how difficult a system actually feels in practice.

Two countries can apply similar withholding taxes while producing very different investor experiences once reclaim procedures, ETF structures, broker integration and reporting obligations are taken into account.

To make those differences easier to visualise, the table below uses a simplified editorial framework focused on investor friction rather than theoretical tax optimisation.

The categories are intentionally broad and investor-oriented. They are designed to compare practical usability, not to create a formal tax ranking or legal classification.

| Country | Withholding Burden | Reclaim Simplicity | ETF Efficiency | Investor Complexity | Overall Friction |

|---|---|---|---|---|---|

| France | High | High | Medium | High | High |

| Denmark | High | High | Low | High | High |

| Germany | Medium | Medium | High | Medium | Medium |

| Italy | Medium | Medium | Medium | Medium | Medium |

| Poland | Medium | Medium | Low | Medium | Medium |

| Greece | Medium | Medium | Low | Low | Medium |

| Croatia | Medium | Medium | Low | Low | Medium |

| Romania | Low | Medium | Low | Low | Low |

| Ireland | Medium | Low | High | Medium | Medium |

| Netherlands | Medium | Medium | High | Medium | Medium |

| Portugal | Medium | Medium | Medium | Medium | Medium |

Several patterns become visible immediately:

- Countries associated with heavier withholding environments often also create higher reclaim complexity.

- ETF-efficient systems are not always low-tax systems, but they can feel operationally smoother for international investors.

- Lower-friction systems tend to matter most for smaller portfolios where reclaim costs and paperwork can outweigh the potential tax savings themselves.

- International investors frequently prioritise predictability and administrative simplicity over theoretical tax optimisation.

The framework also highlights an important reality of modern investing: dividend taxation is no longer only about the country where the company is located. ETF domicile, broker structure, treaty access and cross-border reporting increasingly shape the investor experience.

For many long-term investors, reducing friction across the entire investment structure matters more than chasing the lowest published withholding rate in isolation.

The final section answers some of the most common questions investors still ask about dividend taxation inside the EU.

Should Investors Chase Dividend Yield After Tax?

For long-term investors, the most important dividend number is rarely the headline yield shown on a stock screener or broker dashboard. What ultimately matters is how much income remains after withholding taxes, local taxation, ETF structure and administrative friction are taken into account.

A stock offering a higher published dividend yield can still produce weaker long-term results if reclaim procedures are difficult, withholding taxes are inefficient or ongoing reporting obligations become burdensome.

This is one reason experienced international investors increasingly focus on after-tax yield rather than raw dividend yield alone.

In practice, tax friction changes investment outcomes more than many investors initially expect.

A portfolio exposed to:

- ongoing withholding inefficiencies

- inefficient reclaim systems

- cross-border reporting complexity

- operational friction

- poorly structured international holdings

may become harder to manage efficiently over long holding periods even when the underlying investments themselves perform well.

Administrative burden also matters more than many investors assume. A theoretically efficient structure may become impractical if investors need to manage repeated reclaim forms, residency certifications or ongoing cross-border documentation every year.

This is one reason many European investors increasingly favour simpler international ETF structures over highly fragmented direct dividend portfolios spread across multiple countries.

In some situations, broadly diversified Irish-domiciled UCITS ETFs can produce more efficient long-term after-tax outcomes than traditional high-yield stock strategies once withholding efficiency, treaty interaction and operational simplicity are considered together.

That does not mean dividend investing is becoming less relevant. Dividend income remains an important part of long-term investing for many European households, retirees and passive-income investors.

But modern dividend investing increasingly rewards:

- structural efficiency

- treaty awareness

- ETF understanding

- administrative simplicity

- long-term usability

rather than simply chasing the highest visible yield available on paper.

For many investors, the most sustainable strategy is not necessarily the one producing the highest theoretical dividend income today — but the one that remains tax-efficient, manageable across borders and operationally realistic over time.

What the EU Is Trying to Change

One reason dividend taxation remains frustrating for many investors is that withholding-tax refunds and treaty relief procedures can still feel slow, fragmented and highly administrative across Europe.

The EU has been trying to address part of that problem through the FASTER initiative — short for “Faster and Safer Tax Excess Relief.”

The framework is designed to simplify and modernise parts of the withholding-tax relief process for cross-border investors inside the EU. The broader goal is to reduce administrative friction, improve standardisation and shorten refund timelines that can currently stretch for months.

Among the main areas targeted by the initiative are:

- faster withholding-tax relief procedures

- more standardised investor documentation

- digital tax-residency certification

- improved coordination between EU tax authorities

The reforms are particularly relevant for cross-border investors holding international dividend portfolios through brokers, custodians and ETF structures operating across multiple jurisdictions.

Implementation is expected gradually over the coming years, with major parts of the framework currently planned to apply from 2030.

For investors, the practical takeaway is simple: the reforms reflect growing concern around the administrative complexity of cross-border withholding-tax procedures.

Conclusion

The biggest challenge in EU dividend taxation is rarely understanding a single tax rate. The real complexity comes from understanding how multiple tax systems interact across borders through withholding taxes, tax residence rules, treaties, ETF structures and local reporting obligations.

For investors, this means headline dividend yield is only part of the picture. Two portfolios with similar pre-tax income can produce very different long-term outcomes once withholding efficiency, reclaim procedures and administrative friction are taken into account.

Modern dividend investing inside the EU increasingly rewards investors who understand structure as much as yield.

For long-term investors, after-tax income and administrative simplicity usually matter more than the highest published dividend yield.

Key Takeaways

- Cross-border dividends can involve both source-country withholding tax and residence-country taxation.

- Tax treaties help reduce double taxation, but reclaim procedures can still create significant administrative friction.

- ETF domicile can materially affect after-tax dividend outcomes, particularly for US equity exposure.

- Irish-domiciled UCITS ETFs became widely used partly because of their interaction with international withholding-tax systems.

- Administrative simplicity often matters as much as headline tax rates for long-term investors.

- Broker withholding is not always the investor’s final tax position.

- Tax residence usually matters more than citizenship for dividend taxation.

- Lower-friction structures can become more valuable over long holding periods than chasing the highest visible yield.

- The EU’s FASTER initiative aims to simplify parts of the withholding-tax relief process from 2030 onward.

FAQ

Cross-border dividends can appear to be taxed twice because withholding tax may be deducted in the source country before the investor’s country of tax residence applies its own investment-income rules.

In practice, tax treaties and foreign tax-credit systems are designed to reduce or mitigate that overlap. The complexity usually comes from timing, reclaim procedures and reporting obligations rather than literal double taxation on the full amount.

Withholding tax is a tax deducted before a dividend payment reaches the investor.

The company, custodian or payment chain may withhold part of the dividend at source according to local tax rules. The investor then receives the reduced amount through the broker account.

Cross-border investors often encounter withholding tax before any residence-country taxation is applied.

There is no single “best” dividend-tax country inside the EU because the investor experience depends on more than headline tax rates alone.

In practice, investors also need to consider:

withholding-tax efficiency

reclaim procedures

treaty access

ETF domicile

reporting complexity

tax residence rules

Some systems are perceived as administratively simpler in certain situations, but the final outcome depends heavily on the investor’s overall structure.

In some situations, yes.

If withholding tax was deducted above treaty levels, investors may be eligible to apply for a partial refund from the foreign tax authority.

The reclaim process can involve:

tax residency certificates

broker confirmations

local tax forms

documentation requirements

lengthy processing periods

For smaller portfolios, investors sometimes discover that the administrative burden outweighs the potential refund itself.

ETF taxation can work differently because the fund structure itself may interact with withholding-tax systems before the investor receives any distribution.

Fund domicile, treaty access and internal withholding treatment can all affect long-term after-tax outcomes.

This is one reason Irish-domiciled UCITS ETFs became widely used among European investors building international portfolios.

Different brokers, custodians and intermediary chains do not always apply treaty relief in the same way.

The final withholding amount can depend on:

submitted tax forms

residency documentation

broker structure

custody chain

applicable treaty rates

This is why two investors holding similar assets through different brokers may still receive different net dividend payments.

Not automatically.

Changing countries does not necessarily change tax treatment unless tax residence itself changes as well.

Source-country withholding taxes may still apply, while local reporting obligations, treaty interaction and residence-country taxation can continue affecting the investor after relocation.

For many internationally mobile investors, overall tax friction matters more than simply relocating to a country with lower published dividend-tax rates.

Matias Buće has a formal background in administrative law and more than ten years of experience studying global markets, forex trading, and personal finance. His legal training shapes his approach to investing — with a focus on regulation, structure, and risk management. At Finorum, he writes about a broad range of financial topics, from European ETFs to practical personal finance strategies for everyday investors.

Sources & References

EU regulations & taxation

- European Commission / Taxation & Customs — ETF domicile

- FASTER initiative

- Irish-domiciled UCITS ETFs

- tax residency

- UCITS ETF market

- withholding tax

- Oecd.org — tax treaties