Looking for the best index funds and ETFs in Europe in 2026 means going beyond performance charts and focusing on UCITS structure, costs, taxes, and how these funds actually work across EU countries.

Disclaimer:

The information provided on Finorum is for educational and informational purposes only and does not constitute financial, investment, or tax advice.

Investing involves risk, including the potential loss of capital.

Always conduct your own research or consult a qualified financial advisor before making investment decisions.

Finorum does not promote or endorse any specific financial products or institutions.

INTRODUCTION

In 2026, index funds and ETFs are no longer a niche choice in Europe. They sit at the core of how retail investors actually allocate capital. Assets in European ETFs alone pushed to new records by 2025, crossing well above the three-trillion-dollar mark and reinforcing a shift that looks structural rather than cyclical.

What’s driving it? Cost pressure, regulation, and practicality. For most cross-border mutual funds and ETFs sold to EU retail investors, UCITS has become the default framework — not because it promises higher returns, but because it standardises diversification, custody, disclosure, and investor protection across jurisdictions. That applies whether the exposure is broad, such as pan-European equity benchmarks, or more targeted, including eurozone blue-chip indices and ESG-screened portfolios operating under frameworks like SFDR and ESMA’s ESG fund-naming guidelines.

This is where the real distinction matters. Searching for the best index funds and ETFs in Europe isn’t just about performance tables. It’s about understanding which products are genuinely UCITS-eligible, how costs compound over time, and how national tax rules shape outcomes from one country to another. In practice, those factors tend to matter more in 2026 than the headline index printed on the factsheet.

If you want a broader beginner framework for starting small in Europe, see

How to Invest €1000 in Europe (2026 Guide)

Best European Index Funds 2026: Comparing STOXX, Euro Stoxx 50 and MSCI Europe

STOXX Europe 600 Index Funds: Broad Market Exposure

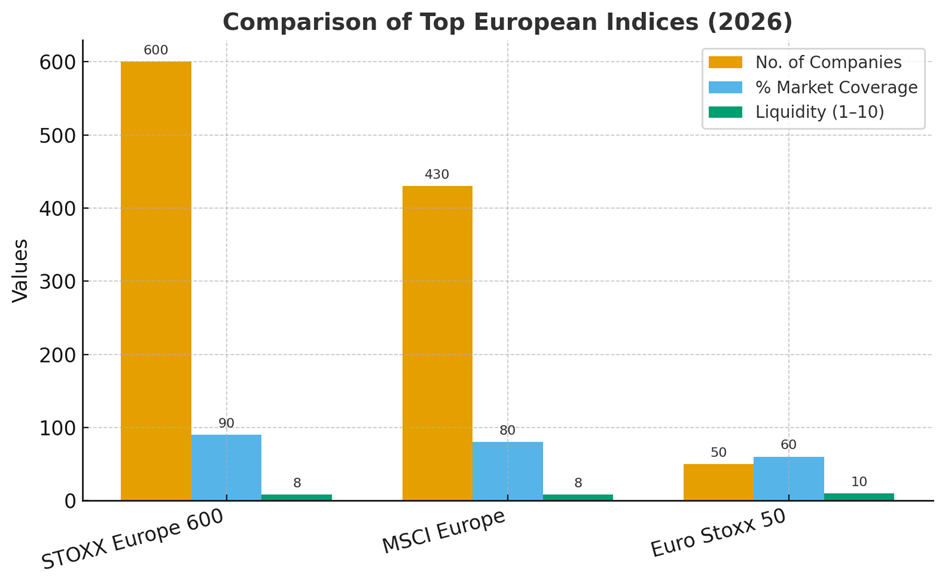

The STOXX Europe 600 is the widest of the three benchmarks. It tracks 600 large-, mid-, and small-cap companies across around 17–18 developed European markets, capturing close to 90% of the region’s free-float market capitalisation.

Breadth comes at a price.

That breadth shows up clearly in the sector mix. In ESG-tilted variants such as the SPDR STOXX Europe 600 SRI UCITS ETF, financials typically rank among the largest sector weights, alongside health care, industrials, and technology — with smaller allocations spread across telecoms, basic materials, real estate, utilities, and energy.

Why investors use it: diversification across market sizes and sectors.

The trade-off: overlap with large-cap names, while small-cap exposure can add volatility — especially noticeable for investors contributing regularly rather than lump-sum investing.

In practice, STOXX Europe 600-based UCITS ETFs account for a significant share of broad European equity allocations.

Euro Stoxx 50 ETFs: Eurozone Blue Chips Only

The Euro Stoxx 50 takes a far more concentrated approach. It includes 50 of the largest and most liquid blue-chip companies from the euro area, weighted by free-float market capitalisation and drawn from roughly eight to twelve eurozone countries.

Concentration cuts both ways.

Household European names such as LVMH, SAP, and TotalEnergies have consistently featured among its largest constituents. Sector exposure reflects that focus: financials, industrials, technology, and consumer-related sectors account for a substantial share of the index, leaving less room for smaller or more defensive segments.

Why investors use it: exceptional liquidity and clear exposure to eurozone corporate leaders.

The risk: concentration — both by sector and by geography — which can amplify drawdowns during eurozone-specific shocks.

Euro Stoxx 50 UCITS ETFs remain a staple in tactical and shorter-horizon European equity strategies.

MSCI Europe ETFs: A Middle Ground

MSCI Europe sits between the two extremes. It covers large- and mid-cap stocks across 15 developed European markets, representing roughly 85% of the free-float market capitalisation and excluding small caps by design. The number of constituents typically fluctuates around 400 as the index is rebalanced.

Stability over completeness.

The result is often a smoother ride than the STOXX Europe 600, without the narrow concentration of the Euro Stoxx 50. For long-term investors building diversified portfolios, this balance tends to reduce volatility without sacrificing regional breadth.

This is precisely why many core European equity UCITS ETFs continue to track MSCI Europe as their primary benchmark.

Strength: broad regional exposure with lower volatility than small-cap-inclusive indices.

Limitation: no participation in European small caps and higher correlation with global developed markets.

Side-by-side comparison of Europe’s main equity benchmarks in 2026. Constituents and market coverage are indicative; MSCI Europe typically includes around 400–430 companies depending on index rebalancing.

Comparing the Main European Equity Benchmarks (2026)

| Index | Companies | Market Coverage | Structural Bias | Typical UCITS ETF | Liquidity |

|---|---|---|---|---|---|

| STOXX Europe 600 | 600 | Large, mid & small cap | Broad, multi-sector | SPDR STOXX Europe 600 UCITS ETF | High |

| Euro Stoxx 50 | 50 | Eurozone large caps only | Concentrated, cyclical tilt | SPDR Euro Stoxx 50 UCITS ETF | Very high |

| MSCI Europe | ~400 | Large & mid caps | Balanced, no small caps | iShares Core MSCI Europe UCITS ETF | High |

If you’re deciding between US and European benchmark exposure in 2026, see

S&P 500 UCITS vs Euro Stoxx 50: A Comparison for 2026

ESG European Index Funds (2026) and the Rise of Sustainable Investing

One of the clearest shifts in European ETF markets is the steady move toward ESG-oriented index funds. This isn’t a branding exercise. Under the EU Taxonomy Regulation and the Sustainable Finance Disclosure Regulation (SFDR), asset managers are required to classify and disclose how sustainability risks and objectives are integrated into their products.

As a result, ESG variants of major benchmarks — including MSCI Europe, STOXX Europe 600, and Euro Stoxx 50 — have become standard offerings within the UCITS ETF universe. Industry data point to strong inflows into sustainable ETFs throughout 2025, alongside a steadily rising share of ESG products within total European ETF assets.

Still, this is where expectations often drift. ESG index funds are not designed to outperform traditional benchmarks by default, nor do they remove sector concentration or cyclical risk. What they primarily change is the rulebook — screening criteria, exclusions, and weighting adjustments — while keeping the underlying index logic intact.

The regulatory framework itself is also evolving. Ongoing discussions around a potential “SFDR 2.0”, including a shift away from the current Article 6/8/9 structure toward a clearer, label-based system, signal that ESG classifications in 2025–2026 remain transitional rather than final. Investors should read ESG labels as regulatory disclosures, not permanent quality stamps.

So what role do ESG European index funds actually play? In most portfolios, they function less as return enhancers and more as alignment tools — allowing investors to express sustainability preferences while preserving diversification, liquidity, and cost discipline typical of broad UCITS index funds.

That distinction is easy to miss. And it matters.

If you want a practical shortlist of ESG options within UCITS, see

Best ESG UCITS ETFs in Europe (2026 Guide)

Risks of European Index Funds in 2026: What Still Matters

Index funds reduce complexity, not risk. Even broadly diversified European ETFs remain exposed to structural factors that investors often underestimate.

Market volatility is the most obvious one. European equity indices can fall sharply during recessions or regional shocks, regardless of how diversified they appear on paper. Currency risk is another. ETFs denominated outside the investor’s home currency introduce FX exposure that can either amplify or dilute returns.

Then come the frictions. Bid–ask spreads, brokerage fees, and tracking differences may look minor in isolation, but they compound over time. Taxes matter even more. Dividend withholding taxes, capital gains rules, and reporting requirements vary significantly by country, as outlined in sources such as PwC Tax Summaries and the KPMG EU Tax Centre.

Finally, there is policy risk. Index methodologies change, sector weights shift, and regulatory updates — from PRIIPs disclosures to MiFID II adjustments — can affect net returns in ways that have nothing to do with market performance.

None of this invalidates index investing. It simply reinforces the need to understand what you own.

How to Build a European Index Fund Portfolio in 2026

There is no single optimal allocation. But simple structures tend to hold up better than complex ones.

A practical approach for many investors is to start with a broad European equity core, add a concentrated blue-chip sleeve, and complement it with a small satellite allocation. In practice, that often means a STOXX Europe 600 ETF as the foundation, a Euro Stoxx 50 ETF for liquidity and large-cap exposure, and a smaller allocation to either an ESG-focused or small-cap UCITS ETF.

Each component plays a role. The broad index delivers diversification across markets and sectors. The blue-chip allocation provides stability and tradability. The satellite position introduces a deliberate tilt — toward sustainability, size, or growth — without dominating overall risk.

Simple. Intentional.

UCITS Regulation and ETF Availability Across Europe

UCITS harmonises fund rules, not market access.

Even when two investors buy the same UCITS ETF, their experience can differ depending on where they live. Listing venues, platform availability, trading costs, and tax treatment vary across countries. A Dutch investor may face different access conditions than a German investor, despite purchasing an identical UCITS product.

UCITS ensures investor protection, diversification rules, and disclosure standards. It does not guarantee that every ETF is equally accessible or cost-efficient in every market.

Checking availability with your broker remains a practical necessity.

If you want the full UCITS framework explained — including why US ETFs don’t qualify for most EU retail investors — see

Why Europeans Can’t Buy US ETFs (PRIIPs Rules Explained)

Low-Cost and Tax-Efficient UCITS ETFs in Europe (2026)

Cost is one of the few variables investors can control. In Europe, UCITS ETFs tracking major equity indices are available with total expense ratios as low as 0.07%–0.12%.

That difference compounds quietly. A €10,000 investment growing at 7% annually reaches nearly €38,700 over 20 years. Add just 0.20% in extra annual fees, and more than €1,500 disappears. No headlines. Just math.

According to justETF data as of late 2025, some of the most cost-efficient European equity index funds include the iShares Core MSCI Europe UCITS ETF, the SPDR STOXX Europe 600 UCITS ETF, and — at a higher cost — MSCI Europe small-cap UCITS ETFs for investors seeking broader exposure.

If you want to understand the real cost gap between platforms (beyond TER), see

Low-Fee vs High-Fee Brokers in Europe

Compared with active equity funds that often charge 1% or more, the difference is structural. Over long horizons, fees tend to matter more than index selection itself.

Illustrative European index fund portfolio for 2026, combining broad UCITS exposure (STOXX Europe 600), eurozone blue chips (Euro Stoxx 50), and a small ESG or small-cap tilt.

Tax Efficiency Matters for European Index Funds

Costs get most of the attention. Taxes usually decide the outcome.

Across the EU, the tax treatment of ETFs varies far more than many investors expect. Reports from firms such as PwC and KPMG consistently show that dividend taxation, capital gains rules, and reporting obligations differ not only by country, but also by product structure and fund domicile. Two investors holding the same ETF can end up with meaningfully different net returns.

This is where net performance starts to diverge.

Dividend and Capital Gains Taxation in Key EU Markets (as of 2025)

| Country | Dividend Tax Treatment | Capital Gains Tax | Practical Notes |

|---|---|---|---|

| Germany | ~26.4% effective (25% + solidarity surcharge) | ~26.4% on sale | UCITS ETFs domiciled in Ireland or Luxembourg can benefit from treaty relief at source, depending on underlying markets |

| Spain | 19% withholding | 19%–26% progressive | ETF income must be declared annually; accumulating share classes reduce cash-flow complexity but not reporting duties |

| Italy | 26% flat tax | 26% flat tax | Accumulating ETFs defer taxation until sale, rather than eliminating it |

| Netherlands | Box 3 deemed return system | Wealth tax (no direct CGT) | Taxed on assumed returns, not actual gains; rules are evolving toward a “real return” model |

| France | 12.8% income tax on dividends (PFU) | 30% flat tax (PFU) | PEA accounts offer significant relief after five years, but only for eligible EU/EEA assets |

Tax rates are indicative for 2025 and exclude special cases such as church taxes, exemptions, or personal allowances.

Why ETF Domicile Often Matters — but Is Not Universal

Even within the UCITS framework, tax efficiency is not uniform. The domicile of the ETF — most commonly Ireland or Luxembourg — affects how dividend withholding taxes are applied at source before returns reach the investor.

Ireland-domiciled UCITS ETFs often benefit from relatively favourable double-taxation treaties, particularly for dividends from large international markets. On a 2% dividend yield, a 10% difference in withholding tax compounds quietly over time. That said, the advantage depends on the underlying holdings and the investor’s local tax regime — Ireland is not automatically “best” in every case.

This distinction is frequently overlooked. And over long horizons, it compounds.

Risks and Practical Considerations Investors Often Miss

Low fees alone do not guarantee tax efficiency.

Local tax law ultimately overrides EU-level harmonisation. Dividend taxation in Spain follows a different logic than in Belgium. The Dutch Box 3 system bears little resemblance to capital gains regimes elsewhere. Rebalancing costs, tracking differences, and withholding taxes can quietly erode returns even in low-TER ETFs.

Regulation also evolves. Updates to MiFID II, ongoing PRIIPs reform, changes to national tax codes, and developments around SFDR all influence how ETFs are taxed and reported. What works well in 2025 may require reassessment later.

Staying informed matters more than chasing perfection.

Investor Reality Check

When evaluating the best index funds and ETFs in Europe, focusing solely on the lowest TER is rarely optimal.

A slightly more expensive ETF that aligns better with your country’s tax framework can deliver higher net returns over time. In practice, this often looks like:

- A German investor favouring Ireland-domiciled UCITS ETFs due to treaty treatment on foreign dividends.

- A Dutch investor prioritising Euronext-listed ETFs for easier access and lower transaction costs.

- A French investor choosing EU-domiciled UCITS ETFs over US-domiciled funds to avoid unnecessary withholding and PFU inefficiencies.

Taxes don’t show up in performance charts. But they compound just like fees.

European Index Funds vs Mutual Funds (2026)

For most of the past few decades, mutual funds were the default investment vehicle across Europe. That balance has shifted. In 2026, UCITS index funds and ETFs dominate new inflows, largely because they combine lower costs with clearer rules on transparency, pricing, and access.

The choice is no longer ideological. It’s practical. Index funds and mutual funds serve different purposes — and understanding the trade-offs matters more than ever.

Key Differences: UCITS Index Funds vs Mutual Funds

| Feature | European Index Funds (UCITS ETFs) | Mutual Funds (Active or Passive) |

|---|---|---|

| Fees (TERs) | Typically ~0.07%–0.30% (broker commissions and custody costs may apply) | ~0.80%–1.50% (active); ~0.20%–0.60% (passive) |

| Tracking Error | Generally low, varies by provider | Often higher, especially in active strategies |

| Transparency | Daily disclosure of holdings | Monthly or quarterly disclosure |

| Trading & Liquidity | Intraday trading on exchanges | Priced once per day at NAV |

| Dividend Handling | Choice between Acc (reinvested) or Dist (paid out) | Usually automatic reinvestment |

| Tax Efficiency | Often favourable under UCITS structures | Highly dependent on domicile and structure |

| Strategy | Passive, index-tracking | Active management or passive |

TER ranges are indicative and based on ESMA’s “Costs and Performance of EU Retail Investment Products” (2024) and the EFAMA Fact Book (2025).

In simple terms, UCITS ETFs are usually three to five times cheaper than the average mutual fund — and far easier to analyse. Over long horizons, that difference tends to dominate outcomes.

Why Investors Continue to Choose Index Funds

Costs come first. And they compound.

A one-percentage-point annual fee difference may not sound dramatic, but over 20 years it can erode more than 20% of total wealth, according to long-term Morningstar data. This is the primary reason passive index funds have gained ground so consistently.

Tracking quality is another factor. Well-managed UCITS ETFs tend to follow their benchmarks closely. Many active mutual funds don’t. After fees, deviations from the index often work against the investor.

Accessibility also matters. UCITS ETFs are widely available through European brokers, typically without minimum investment requirements. Add in strong regulatory oversight under the UCITS framework — standardised reporting, diversification rules, and cross-border portability — and the appeal becomes obvious.

Finally, flexibility. ETFs allow investors to choose between accumulating share classes, which reinvest dividends automatically, and distributing classes, which pay them out. Mutual funds usually reinvest by default, but the tax treatment can differ materially.

This is where details start to matter.

When Mutual Funds Still Make Sense

Index funds are not a universal solution.

Active management can still play a role in specific areas, such as niche sectors, smaller markets, or strategies where index construction is less efficient. In some countries, local tax rules may also favour certain mutual fund structures over ETFs.

Convenience is another factor. For investors who prefer automatic investment plans without trading on exchanges, traditional mutual funds can feel simpler — even if they are more expensive.

That said, style drift remains a risk. Active funds do not always stick closely to their stated mandate, which can quietly change the risk profile of a portfolio over time.

Risks and Considerations Investors Often Overlook

Performance dispersion is real. Over ten-year periods, more than 75% of actively managed European equity funds have underperformed their benchmarks after costs, depending on category and period, according to Morningstar.

Fees are the main culprit, but not the only one. Entry and exit fees, custody charges, and brokerage commissions can reduce returns even in low-TER ETFs. Availability also varies. Many mutual funds are distributed only domestically, limiting access for cross-border investors.

Regulation adds another moving part. Updates to MiFID II, PRIIPs disclosures, and product-labelling rules can influence how funds are sold, reported, and accessed across Europe.

None of this invalidates either structure. It simply reinforces the need to understand how each one actually works.

Investor Reality Check: Combining Both Approaches

For most long-term investors, low-cost European index funds remain the most efficient foundation. But that doesn’t exclude active funds entirely.

A common compromise is the core–satellite approach:

- Core (≈70%): UCITS ETFs tracking broad European equity indices

- Satellite (≈20%): Select active mutual funds targeting specific niches (for example, small caps or infrastructure)

- Satellite (≈10%): ESG or thematic funds aligned with long-term trends

The logic is straightforward. Keep costs low where markets are efficient. Take selective, measured risk where active management may add value.

Simple. Disciplined. Realistic.

Case Studies: How EU Investors Use European Index Funds in 2026

European index funds may track the same benchmarks, but how they are used in practice varies sharply by country. Taxes, account structures, and market access shape real portfolios far more than index labels.

Here’s how that plays out across key EU markets.

Germany: Building a Tax-Aware UCITS Core

Germany is Europe’s largest ETF market by assets. By mid-2025, German investors held around €500 billion in ETFs, including both retail and institutional assets, according to industry data. Household participation continues to grow, driven in large part by long-running ETF savings plans (ETF-Sparpläne).

Most long-term portfolios are anchored in low-cost UCITS ETFs domiciled in Ireland or Luxembourg, reflecting both product availability and the interaction between withholding taxes, treaty relief, and Germany’s investment tax framework.

Illustrative allocation:

- 70% iShares Core MSCI Europe UCITS ETF (Acc) — large- and mid-cap core exposure

- 20% SPDR STOXX Europe 600 UCITS ETF (Acc) — added breadth, including small caps

- 10% Xtrackers MSCI Europe Small Cap UCITS ETF — growth tilt

Accumulating share classes are commonly preferred. Dividends are reinvested automatically inside the fund, supporting long-term compounding and reducing repeated taxable cash flows under the German system.

Regulatory watch (Germany): PRIIPs rules require a Key Information Document (KID) before UCITS ETF purchases; ESMA guidance remains the primary reference.

Spain: Managing Dividend Withholding and ESG Preferences

Spanish investors often value dividend income but face a 19% withholding tax at the distribution stage. Capital gains and dividend income are ultimately taxed under the savings tax scale, which rises progressively depending on total income.

To limit repeated cash taxation, many portfolios lean toward accumulating UCITS ETFs or ESG-tilted strategies aligned with domestic sustainability preferences.

Illustrative allocation:

- 60% STOXX Europe 600 UCITS ETF (Acc)

- 25% MSCI Europe ESG Leaders UCITS ETF (Acc)

- 15% Euro Stoxx 50 UCITS ETF (Acc)

At the initial withholding stage, a €1,000 dividend typically triggers around €190 in tax. Additional tax may apply when income is declared annually, depending on the investor’s total savings income. Accumulating ETFs avoid repeated distributions, even though income must still be reported.

Regulatory watch (Spain): CNMV guidance governs UCITS reporting and disclosure requirements.

Italy: Accumulating Classes and Long-Term Compounding

Italy applies a flat 26% tax on most financial income, including dividends and capital gains. As a result, Italian investors often prioritise tax deferral and administrative simplicity.

Illustrative allocation:

- 65% MSCI Europe UCITS ETF (Acc)

- 20% STOXX Europe 600 UCITS ETF (Acc)

- 15% European small-cap or quality-factor ETF

A simple illustration shows why. A €1,000 dividend becomes €740 after tax. When dividends are reinvested via accumulating share classes instead of being distributed and taxed each year, the difference compounds over time — often reaching several thousand euros over a decade.

Regular contributions through dollar-cost averaging are also widely used to smooth volatility.

Regulatory watch (Italy): Updates from the Ministry of Economy and Finance remain the primary reference for tax treatment.

Netherlands: Costs, Access, and Box 3 Awareness

The Dutch system follows a different logic. Under Box 3, investors are taxed on a deemed return rather than actual realised gains. This places greater emphasis on low costs, clean reporting, and operational efficiency.

Euronext-listed UCITS ETFs are popular for euro denomination, liquidity, and relatively tight spreads.

Illustrative allocation:

- 70% STOXX Europe 600 UCITS ETF (Acc)

- 20% MSCI Europe UCITS ETF (Acc)

- 10% thematic or ESG satellite ETF

In practice, Box 3 taxation may apply even in years of modest or negative performance. However, recent reforms allow investors, in certain cases, to claim taxation based on a lower actual return rather than the standard deemed rate. This makes cost control especially important under the current transition regime.

Regulatory watch (Netherlands): Box 3 reforms remain ongoing; investors should monitor updates from the Belastingdienst.

France: Leveraging PEA Accounts and UCITS Breadth

France offers a distinct advantage through the Plan d’Épargne en Actions (PEA). When held for at least five years, PEA accounts provide significant tax relief — but only for eligible EU and EEA assets and qualifying fund structures.

Many investors therefore combine PEA-eligible UCITS ETFs with additional holdings outside the wrapper.

Illustrative allocation:

- 70% PEA-eligible MSCI Europe or STOXX Europe 600 ETF (Acc)

- 20% Euro Stoxx 50 UCITS ETF (Acc)

- 10% ESG or thematic ETF outside PEA

Eligibility is the key constraint. Not all UCITS ETFs qualify for PEA treatment, even if they track European indices.

Investor reminder: Always confirm PEA eligibility before purchase.

All allocations shown are illustrative examples only and do not constitute personalised investment advice. Actual outcomes depend on individual circumstances, tax residency, and applicable regulations.

How to Start with European Index Funds (Step by Step, 2026)

Getting started with European index funds is less about picking the “perfect” ETF and more about getting the structure right. The sequence matters.

Here’s a practical way to approach it in 2026.

- Define your objective

What is this money for?

Retirement, a future home purchase, or long-term wealth accumulation all imply different time horizons and risk tolerance. A 30-year horizon can absorb volatility. A 5-year horizon usually can’t.

Be honest here. Everything else builds on this. - Choose your benchmark

Before choosing an ETF, choose the index it tracks.

Broad exposure comes from benchmarks like the STOXX Europe 600. A large- and mid-cap blend points toward MSCI Europe. A pure blue-chip tilt means Euro Stoxx 50. Sustainability preferences can be expressed through ESG variants of these indices.

For most beginners in 2026, broad UCITS ETFs tracking STOXX Europe 600 or MSCI Europe remain the safest starting point.

Simple beats clever at this stage. - Select the UCITS ETF

Once the benchmark is clear, the ETF selection becomes technical.

Compare total expense ratio (TER), tracking error, fund domicile, liquidity, and typical bid–ask spreads. Then look at the share class. Accumulating (Acc) ETFs reinvest dividends automatically, while distributing (Dist) ETFs pay them out.

Always read the factsheet. Index methodology and rebalancing frequency matter more than marketing labels. - Pick a broker and calculate the real cost

TER is only part of the picture.

Broker commissions, custody or inactivity fees, FX mark-ups, and entry or exit charges can easily add several dozen basis points per year. Two investors holding the same ETF through different brokers can end up with very different net returns.

It’s also worth checking whether the broker supports fractional shares and automated investment plans. Both are becoming more common across Europe and make it much easier to start small and invest regularly.

This step is often underestimated. It shouldn’t be. - Start small and diversify

You don’t need a large lump sum to begin.

A simple example might be €1,000 split between a broad European ETF and a more concentrated blue-chip index. From there, regular contributions through monthly or quarterly investing smooth entry points and reduce timing risk.

Consistency usually matters more than precision. - Automate reinvestment

Automation removes friction.

Accumulating share classes reinvest dividends inside the fund without any action required. Distributing ETFs can still work, but they require manual reinvestment or deliberate payout planning — and may create additional tax events.

For long-term compounding, automation helps more than most people expect. - Monitor, don’t micromanage

Index funds don’t need constant attention.

A quarterly check to confirm allocations and an annual rebalance are usually sufficient. Beyond that, the main things to watch are external: regulatory changes at EU level. Disclosure and labelling rules under PRIIPs and sustainability frameworks such as SFDR are evolving through 2025–2026, alongside ongoing MiFID II updates, and can influence how products are classified and sold.

Markets move. Rules change. Portfolios should adjust — slowly.

If you want a beginner-focused broker shortlist for Europe in 2026, see

Best Brokers in Europe for Beginners (2026)

Professional perspective

For investors dealing with cross-border accounts, multiple tax regimes, or larger portfolios, professional advice can be worthwhile. A licensed financial adviser or tax professional in your country can help ensure compliance and optimise after-tax outcomes.

Especially in Europe, details matter.

Conclusion: What Actually Matters in 2026

European index funds have matured. In 2026, the challenge is no longer access or product choice — it’s decision quality.

UCITS ETFs tracking broad European indices are widely available, inexpensive, and heavily regulated. That part is largely solved. What still separates outcomes is how investors deal with costs beyond TER, tax treatment across countries, and the practical details of implementation.

The uncomfortable truth is that many underwhelming results have little to do with markets. They come from avoidable frictions: choosing the wrong share class, ignoring fund domicile, overpaying on broker costs, or misunderstanding local tax rules. None of these show up in index performance charts, but all of them compound over time.

There is also no single “best” European index fund. A structure that works well for a German investor using accumulating UCITS ETFs may be inefficient for a Dutch investor under Box 3 or a French investor investing through a PEA wrapper. In Europe, optimisation is local by default.

Index investing still works. But only when it is treated as a system, not a product.

Key Takeaways

- UCITS is the baseline. For EU retail investors, UCITS-compliant index funds and ETFs remain the safest and most transparent way to access European equities.

- Costs go beyond TER. Broker fees, spreads, FX charges, and tax leakage often matter more than small differences in headline expense ratios.

- Taxes are not uniform. Dividend and capital gains taxation varies widely across EU countries and can materially change net returns.

- Share class choice matters. Accumulating and distributing ETFs lead to very different cash flows and tax outcomes.

- Domicile affects efficiency. Ireland- and Luxembourg-domiciled UCITS ETFs often reduce withholding tax friction, but not universally.

- ESG labels are evolving. SFDR classifications and sustainability disclosures are changing through 2025–2026 and should be treated as transitional.

- Simplicity scales better. Broad indices, regular contributions, and limited rebalancing tend to outperform complex strategies in real life.

- “Best” is country-specific. What works in Germany may not work in Spain, the Netherlands, or France.

If you get those details right, the index itself usually takes care of the rest.

Frequently Asked Questions (FAQ): European Index Funds & ETFs (2026)

There is no single best option for all investors. In practice, broad UCITS ETFs tracking indices such as STOXX Europe 600 or MSCI Europe remain the most common core choices in 2026 due to diversification, low costs, and wide availability across EU countries.

For EU retail investors, UCITS ETFs are generally safer and more transparent. They follow strict diversification rules, custody requirements, and disclosure standards under EU law, which non-UCITS funds do not always meet.

Accumulating (Acc) ETFs reinvest dividends automatically inside the fund, while distributing (Dist) ETFs pay dividends out to investors. The choice affects cash flow, taxes, and long-term compounding, especially across different EU tax systems.

Taxation varies by country. Dividend withholding taxes, capital gains tax, and reporting rules differ between Germany, Spain, Italy, France, the Netherlands, and others. Two investors holding the same ETF can face very different net returns depending on tax residence.

ETF domicile affects withholding tax treatment at source, especially on foreign dividends. Ireland- and Luxembourg-domiciled UCITS ETFs often reduce dividend leakage through tax treaties, but the benefit depends on the underlying assets and the investor’s local tax rules.

ESG index funds allow investors to align portfolios with sustainability preferences while keeping costs low. However, ESG ETFs are not designed to outperform by default. SFDR classifications and naming rules are evolving through 2025–2026, and investors should review the latest SFDR and proposed “SFDR 2.0” guidance to understand what an ESG label actually implies.

Over long periods, most active European equity funds underperform their benchmarks after fees, depending on category and timeframe. Lower costs and consistent market exposure explain why index funds dominate long-term outcomes for many investors.

Yes. Many European brokers now support fractional shares and automated investment plans, allowing investors to start with small amounts and invest regularly. This makes index investing accessible even without large upfront capital.

For most investors, annual rebalancing is sufficient, with occasional quarterly checks. Over-monitoring often leads to unnecessary trades and higher costs without improving results.

Yes — when implemented correctly. Broad diversification, low costs, tax awareness, and discipline make European index funds well suited for long-term wealth building, provided investors account for local tax rules and regulatory changes.

Matias Buće has a formal background in administrative law and more than ten years of experience studying global markets, forex trading, and personal finance. His legal training shapes his approach to investing — with a focus on regulation, structure, and risk management. At Finorum, he writes about a broad range of financial topics, from European ETFs to practical personal finance strategies for everyday investors.

Sources & References

EU regulations & taxation

- Economie.gouv.fr — PFU

- European Commission / Taxation & Customs — Costs and Performance of EU Retail Investment Products” (2024)

- ESMA’s ESG fund-naming guidelines

- investor protection

- MiFID II

- PRIIPs

- SFDR

- UCITS-eligible

- UCITS structure

- Oecd.org — withholding tax

- PwC Tax Summaries — PwC

- Taxfoundation.org — Germany

Additional educational resources

- Belastingdienst.nl — Netherlands

- Blackrock.com — iShares Core MSCI Europe UCITS ETF

- Efama.org — EFAMA Fact Book (2025)

- Etf.dws.com — Xtrackers MSCI Europe Small Cap UCITS ETF

- Euronext.com — Euronext

- justETF

- Morningstar

- Msci.com — MSCI Europe

- Sede.agenciatributaria.gob.es — Spain

- Service-public.gouv.fr — PEA

- Ssga.com — SPDR STOXX Europe 600 SRI UCITS ETF

- Stoxx.com — Euro Stoxx 50

- STOXX Europe 600