In this guide, we break down the key differences in the Global vs European ETFs debate and explain which option works best for long-term European investors.

Disclaimer:

The information provided on Finorum is for educational and informational purposes only and does not constitute financial, investment, or tax advice.

Investing involves risk, including the potential loss of capital.

Always conduct your own research or consult a qualified financial advisor before making investment decisions.

Finorum does not promote or endorse any specific financial products or institutions.

Introduction: Global vs European ETFs for European Investors

Exchange-traded funds (ETFs) have become one of the most accessible and widely used investment tools in Europe, thanks to their low costs, transparency, and broad market exposure. But one question continues to surface for new and experienced investors alike: should Europeans rely on global ETFs, or are European UCITS ETFs ultimately the better choice?

The answer isn’t straightforward. Global ETFs often offer wider diversification and deep liquidity, especially those listed in the US. Meanwhile, European UCITS ETFs come with clear tax efficiencies, stronger investor protections, and a regulatory framework designed specifically for EU-based savers. For many investors in Europe, the real difference becomes visible only when you look beyond fees.

Recent trends point in a clear direction. According to PwC, European-domiciled ETFs attracted more than €150 billion in net inflows during 2024, while US-listed ETFs saw net outflows — a shift that reflects growing global confidence in the UCITS framework.

In this guide, we break down the most important factors in the debate Global vs European ETFs — costs, taxes, regulation, diversification, and long-term performance. The analysis draws on insights from justETF, ETFtrends, AXA IM, Bajaj AMC, and research published by leading consultancies such as Oliver Wyman and PwC.

By the end, you’ll have a clear sense of which type of ETF — UCITS ETFs vs US ETFs for Europeans — fits your strategy best in 2026 and beyond.

If you’re starting from the basics and want to see how ETFs fit into a beginner portfolio in Europe, see

How to Invest €1000 in Europe (2026 Guide)

ETF Costs in Europe: Global vs UCITS ETFs

Costs are often underestimated by beginners, but for long-term European investors they can quietly become one of the biggest differentiators in performance. Even small frictions — a few basis points of fees, FX spreads, or dividend withholding — compound over time. And in the comparison between Global vs European ETFs, these details often matter more than headline expense ratios.

For most EU-based investors, the cost question comes down to three areas: management fees (TERs), currency conversion, and the real-world accessibility of global vs UCITS ETFs.

Management Fees (TERs)

Global ETFs — especially those listed in the US — built their reputation on ultra-low costs.

A US-domiciled S&P 500 ETF can have a TER as low as 0.03% (Morningstar).

European UCITS equivalents tracking the same benchmark usually fall between 0.07% and 0.15% (justETF). The difference looks small on paper, but TER is only one piece of the full cost picture.

Currency Conversion Costs

Euro-based investors buying US ETFs must deal with USD conversions.

Deposits, trades and withdrawals typically incur a spread of 0.10% to 0.50% per conversion (DEGIRO, Interactive Brokers).

UCITS ETFs with an EUR share class remove this layer entirely — you buy and sell in euros, while the fund handles foreign-exchange exposure internally.

Broker Fees and Accessibility

Access itself can turn into a cost.

- Many European brokers block US-domiciled ETFs because they lack the PRIIPs-required KID documentation.

- UCITS ETFs are widely supported across Europe and often appear on zero-commission ETF lists or monthly savings plans.

For most retail investors, that makes UCITS ETFs not just easier to buy — but cheaper to maintain.

Example Comparison: S&P 500 ETFs

If you want a deeper comparison between the two main benchmarks European investors often choose, see

S&P 500 UCITS vs Euro Stoxx 50: A Comparison for 2026

| Feature | US-Domiciled S&P 500 ETF | UCITS S&P 500 ETF |

|---|---|---|

| Typical TER | 0.03% | 0.07–0.15% |

| Currency Base | USD | EUR / USD |

| FX Costs (EUR investor) | 0.10–0.50% per trade | None (EUR share class) |

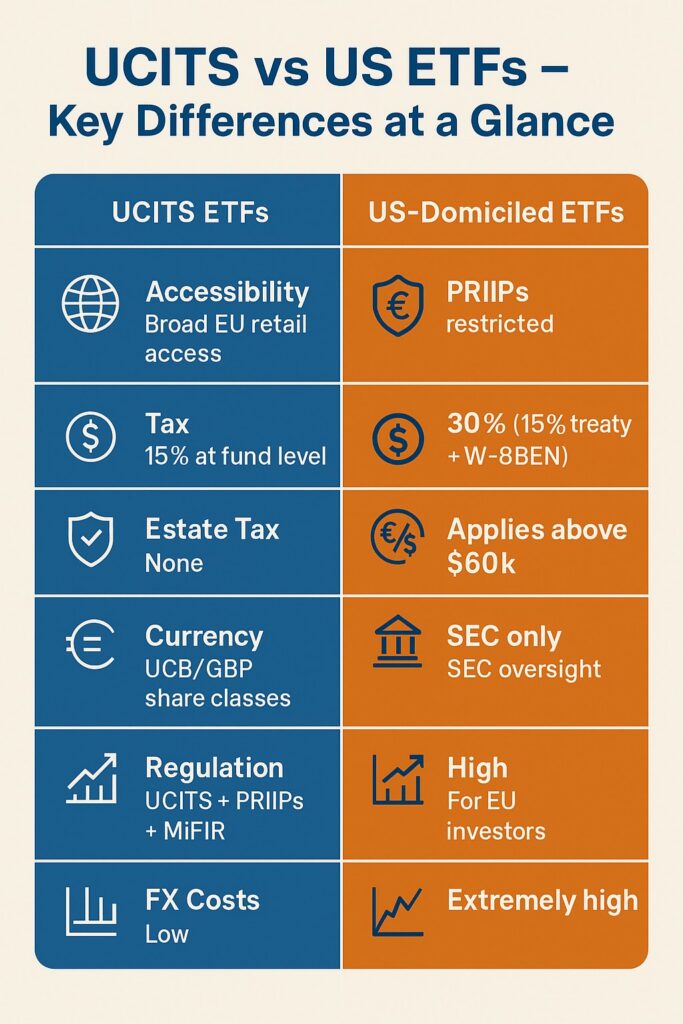

| Dividend Withholding Tax | 30% (15% with treaty & W-8BEN) | 15% automatically at fund level |

| Estate Tax Risk | Yes (above $60k) | None |

| Accessibility | Limited (PRIIPs) | Broad EU retail availability |

| Tax impact (net dividends) | Lower net income after US withholding | Higher net income via Ireland/Luxembourg treaties |

Why Costs Matter More Than They Seem

A US ETF may look cheaper at first glance — 0.03% vs 0.07% TER — but TER alone rarely tells the full story. Once you add:

- FX spreads on every EUR → USD → EUR cycle,

- higher dividend withholding,

- estate-tax exposure above $60,000,

- and limited access for retail investors in Europe,

the apparent advantage of global US ETFs begins to shrink.

A simple example:

A euro-based investor who rebalances twice a year might pay FX spreads four times annually. Over a decade, that single factor can outweigh the entire TER difference between a US ETF and its UCITS counterpart — even before taxes are considered.

For most long-term European investors, UCITS ETFs tend to deliver better net results, not because they are perfect, but because they minimise these frictions consistently over many years.

UCITS vs US ETFs: Investor Protection in Europe

When comparing Global vs European ETFs, regulation is more than a technical point — it determines what European investors can access, how their money is protected, and how transparent their investments really are. For many EU-based savers, the regulatory framework becomes a deciding factor, often outweighing fees or index choice.

UCITS: The Gold Standard in Europe

The UCITS Directive is the backbone of the European ETF market and is widely regarded as one of the most robust investor-protection regimes in global finance. A UCITS ETF must:

- diversify its holdings (no single issuer may exceed 10% of the fund),

- publish consistent, clear reporting,

- safeguard client assets through independent custodians and strict asset segregation.

These safeguards have made UCITS the dominant structure in Europe. As of 2024, more than 75% of all ETFs listed in Europe are UCITS-compliant (PwC). The framework is so widely respected that many institutional investors outside Europe treat UCITS funds as a global benchmark for governance and transparency.

This regulatory strength also stands in sharp contrast to the limitations European investors face under PRIIPs.

PRIIPs Regulation: Why US ETFs Are Blocked

If you want a full explanation of how PRIIPs rules affect ETF access in Europe, see

Why US ETFs Are Restricted in Europe (PRIIPs Rules Explained)

The PRIIPs regulation, in place since 2018, requires all packaged investment products sold to European retail investors to provide a standardised Key Information Document (KID). Most US ETF providers — including Vanguard and the US-domiciled iShares range — do not produce PRIIPs-compliant KIDs.

The result:

- Most European brokers block retail access to US ETFs.

- Retail use of US ETFs in Europe dropped by over 90% once PRIIPs came into force (KPMG).

This is why so many Europeans search for popular tickers like VOO or VTI, only to discover they can’t buy them through their local broker. The restriction isn’t technical — it’s regulatory.

MiFIR and Market Transparency

The Markets in Financial Instruments Regulation (MiFIR) further strengthens transparency in Europe’s ETF market. It enforces post-trade reporting, best-execution requirements and mandatory cost disclosures — all of which help reduce hidden fees and ensure fairer treatment for retail investors.

Governance and Investor Rights

The regulatory contrast becomes even clearer when comparing frameworks side by side:

| Aspect | UCITS ETFs (Europe) | US ETFs (Global) |

|---|---|---|

| Disclosure | KID + structured reporting | Prospectus + SEC filings |

| Investor Protection | Diversification rules, custodians, strict asset segregation | Strong SEC oversight, different governance model |

| Accessibility (EU retail) | Broad EU access | Restricted due to PRIIPs |

| Global Recognition | Very high; widely used outside EU | Extremely high, but limited EU retail availability |

For most European investors, UCITS isn’t just a regulatory label — it’s the framework that determines what you can buy, how well you’re protected, and how clearly your costs and risks are presented. In the debate Global vs European ETFs, regulation often tilts the scales decisively toward UCITS for everyday investors.

UCITS vs US ETFs Taxation: How European Investors Are Affected

For many European investors, taxation isn’t just a footnote in the debate Global vs European ETFs — it’s often the single factor that ultimately tips the scales. While a US-listed ETF may appear cheaper at first glance, experience shows that withholding taxes, estate-tax exposure and administrative complexity can quietly erode returns over time. UCITS ETFs, by contrast, are designed specifically to minimise these frictions for EU-based savers.

Withholding Taxes on Dividends

Dividends are where the first major gap typically emerges.

- US-domiciled ETFs: Non-US investors face a default 30% withholding tax on dividends. Some EU investors can reduce this to 15% by filing a W-8BEN form under a double taxation treaty — but only if the paperwork is correct and kept up to date (BNY Mellon).

- UCITS ETFs holding US stocks: The fund itself claims the treaty rate. Ireland- and Luxembourg-domiciled ETFs generally achieve 15% withholding automatically, sparing investors from any administrative burden (Banker on Wheels).

Experience shows that this small percentage difference compounds meaningfully.

For example:

On a €100,000 investment yielding 3% (€3,000 per year), paying 30% withholding (€900) versus 15% (€450) allows a UCITS investor to keep an extra €450 annually — without filing a single form.

Over long horizons, that adds up to thousands of euros.

Estate Tax Risks

One of the least understood — yet most significant — risks of US ETFs for Europeans is US estate tax.

Non-US residents holding more than $60,000 in US-situs assets, including US-domiciled ETFs, may be subject to estate tax rates that can reach up to 40% (Highgate).

UCITS ETFs sidestep this entirely. Funds domiciled in Ireland or Luxembourg are not considered US assets, meaning European investors face zero estate-tax risk — an advantage many retail investors value even more than tax efficiency.

Tax Reporting Complexity

The administrative differences are also stark:

- US ETFs: Investors must often complete W-8BEN forms and may need to navigate more complex domestic reporting when claiming treaty benefits.

- UCITS ETFs: Reporting is standardised across Europe. The fund handles cross-border taxation, and investors receive simple, consistent documentation.

For most Europeans, especially beginners, this simplicity is a major practical advantage.

Example Comparison: €100,000 Investment in a US Equity ETF

| Factor | US-Domiciled ETF | UCITS ETF (Ireland/Luxembourg) |

|---|---|---|

| Dividend Withholding Tax | 30% (or 15% with treaty) | 15% (handled at fund level) |

| Estate Tax Risk | Yes (>$60,000) | None |

| Reporting Complexity | High | Low |

| After-Tax Dividend (3% yield) | ~2.55% (with treaty) | ~2.55% (net of UCITS handling) |

| Accessibility | Limited (PRIIPs) | Broad EU access |

The Irish Domicile Advantage

Ireland’s tax treaty with the United States is one of the most favourable in the world for investment funds. This is why nearly all major ETF providers — including iShares, Vanguard and SPDR — structure their European product ranges in Ireland.

For European investors, the benefits are clear:

- US withholding tax automatically reduced from 30% to 15%,

- no W-8BEN or treaty paperwork,

- no US estate-tax exposure,

- cleaner, more predictable net returns.

In practice, this means UCITS ETFs often match — or outperform — the after-tax returns of US ETFs, despite slightly higher headline TERs.

National Tax Variations

While UCITS simplifies taxation at the fund level, local rules still vary across Europe.

Examples:

- Germany applies the Vorabpauschale (advance lump-sum tax).

- Italy, Spain and others have their own dividend tax policies.

- Some countries offer tax-advantaged accounts that further shape outcomes.

Investors should therefore always check local tax rules or seek advice, even when using efficient UCITS structures.

Case Study: German Investor with €100,000 in US vs UCITS ETF

- Investment: €100,000 in an S&P 500 ETF

- Dividend yield: 3% (€3,000 annually)

US-Domiciled ETF

- 30% withholding (€900), or 15% (€450) with W-8BEN

- Estate-tax exposure above $60,000

- FX exposure (USD)

- Limited access due to PRIIPs

UCITS ETF (Ireland)

- Withholding automatically reduced to 15% (€450)

- No estate-tax exposure

- EUR share class reduces FX risk

- Clean, simple reporting and full retail access

Outcome

The German investor keeps €450 more per year, avoids estate-tax uncertainty entirely, and faces far fewer administrative hurdles by choosing a UCITS ETF over a US-domiciled equivalent.

For many European savers, experience shows that these practical advantages matter far more over time than a few basis points of TER.

ETF Liquidity in Europe: UCITS vs US ETFs Compared

Liquidity isn’t just about volume — it’s about how easily an investor can get fair execution during their local market hours. In the debate Global vs European ETFs, experience shows that these practical details often matter just as much as fees or index exposure. For European investors, differences in trading windows, spreads and accessibility can subtly influence real-world execution quality.

Trading Hours and Market Coverage

Trading hours alone create a meaningful gap.

- US ETFs: Trade during US market hours (15:30–22:00 CET), which limits the ability of European investors to trade in the morning or early afternoon.

- UCITS ETFs: Trade throughout the European business day. Listings on Xetra (09:00–17:30 CET), Euronext (09:00–17:40 CET) and the London Stock Exchange (08:00–16:30 CET) allow investors to trade when European markets are active.

Experience shows this timing advantage makes portfolio rebalancing, reacting to European news, or placing limit orders far more convenient for EU-based investors.

Bid-Ask Spreads and Liquidity

Liquidity looks very different on each side of the Atlantic.

- US ETFs: Benefit from exceptional scale.

The SPDR S&P 500 ETF (SPY) often trades more than €20 billion per day, with spreads as tight as 0.01%. - UCITS ETFs: Volumes are lower, but for major funds still very efficient.

The iShares Core S&P 500 UCITS ETF (CSPX) typically trades with spreads of 0.05–0.10%, narrow enough that most retail investors won’t notice a practical difference. - Smaller or niche UCITS ETFs: Can have wider spreads, which increases transaction costs — something to keep in mind when buying thematic or low-volume funds.

Tracking Error Considerations

- US ETFs: Often achieve extremely low tracking error due to scale, structure and longer trading windows.

- UCITS ETFs: May show slightly higher tracking error driven by dividends, tax treatment and European trading hours.

For core indices like S&P 500 or MSCI World, the difference is typically just a few basis points.

For long-term buy-and-hold investors, these variations are usually negligible.

Accessibility

This is where the biggest practical gap opens:

- UCITS ETFs: Fully accessible to European retail investors and widely integrated into European brokers and savings plans (e.g., German ETF Sparpläne).

- US ETFs: Restricted for EU retail investors because of PRIIPs KID rules, leading many beginners to discover they cannot buy well-known tickers like SPY or QQQ through their European broker.

Example Comparison: US vs UCITS S&P 500 ETFs

| Factor | US ETF (SPY) | UCITS ETF (CSPX) |

|---|---|---|

| Trading Hours | 15:30–22:00 CET | 09:00–17:30 CET |

| Avg. Daily Volume | €20+ billion | €200–500 million |

| Typical Spread | ~0.01% | ~0.05–0.10% |

| Accessibility (EU retail) | Restricted (PRIIPs) | Broadly available |

For most European investors, UCITS ETFs provide all the liquidity they need — without the access restrictions or timing challenges of US-domiciled ETFs.

If you want to explore some of the most widely used UCITS ETFs available to European investors today, see

Best UCITS ETFs in Europe (2026)

Performance and Diversification: Global vs European ETFs

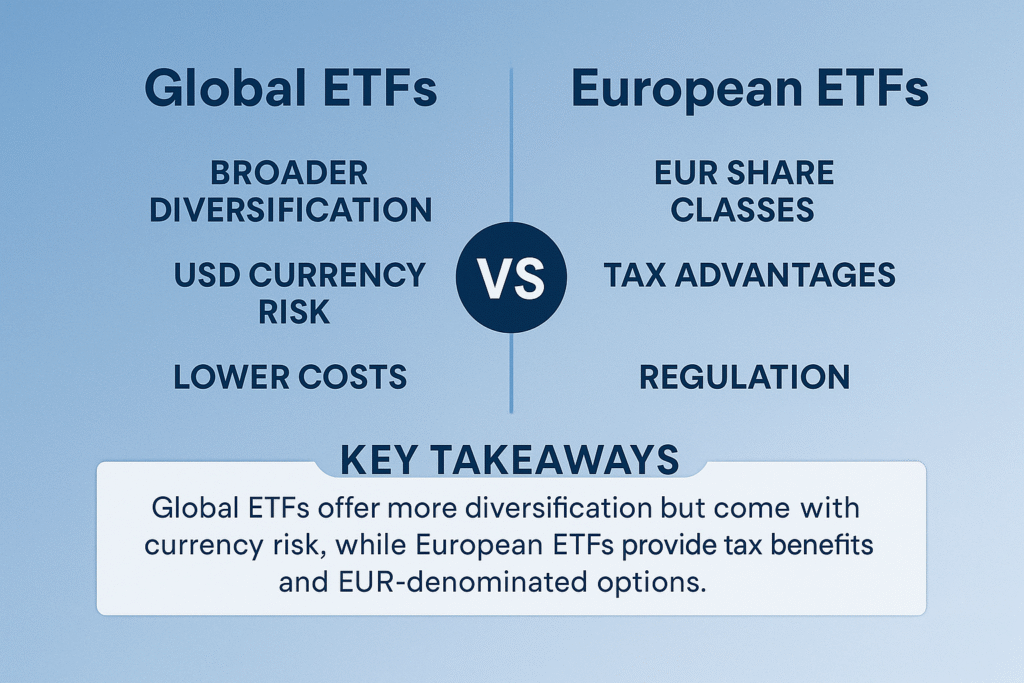

Beyond costs, liquidity and regulation, most investors ultimately care about two things: performance and diversification. In the debate Global vs European ETFs, the real question becomes how much global exposure you want and how comfortable you are with currency risk. Experience shows that these two variables often influence long-term outcomes more than TER differences or fund domicile.

A visual overview of the main distinctions between global and European ETFs, showing how diversification, currency risk and tax treatment influence long-term outcomes for EU-based investors.

Geographic Diversification

Global exposure is where many investors start their comparison.

- Global ETFs (often US-listed): These typically track broad indices like MSCI ACWI or MSCI World, covering the US, Europe, Asia and emerging markets. A single ETF can give exposure to more than 1,500 companies across 20-plus countries, making it one of the simplest ways to build wide diversification.

- European UCITS ETFs: Many UCITS products track the same global benchmarks, but European providers also offer regional exposures such as Euro Stoxx 50, DAX or other pan-European indices. This appeals to investors who want alignment with the European economy or who wish to capture policy-driven opportunities in the EU.

In practical terms, both global US ETFs and global UCITS ETFs offer nearly identical diversification. For most investors, the more meaningful difference lies in currency management.

Currency Risk

Currency movements can have a noticeable impact on returns.

- US ETFs: Usually denominated in USD, exposing Europeans to EUR/USD fluctuations. A 10 percent currency move can materially alter yearly returns, even when the index performs steadily.

- UCITS ETFs: Frequently offer EUR-denominated or currency-hedged share classes that reduce FX volatility. This makes long-term planning smoother and often more predictable for European investors.

For many long-term savers, the unpredictability of currency swings can feel riskier than a few extra basis points of TER. This becomes especially clear when comparing long-term results for the same global index.

Case Study: MSCI World – US vs UCITS

- US MSCI World ETF: Tracks around 1,500 global stocks, USD-denominated, TER roughly 0.12 percent.

- UCITS MSCI World ETF (e.g., iShares IWDA, Vanguard VWCE): Tracks the same index, TER around 0.20 percent, offered in EUR and GBP share classes.

Historical performance from 2015 to 2024 illustrates the point:

- MSCI World Index returned about 9 percent annually in USD.

- UCITS equivalents returned about 8.7 percent annually in EUR.

The difference was driven primarily by currency movements, not structural differences between US and UCITS funds.

If you want a broader look at European index strategies and benchmarks, see

Best European Index Funds (2026)

Sector and Thematic Opportunities

The thematic landscape offers another point of differentiation.

- US/global ETFs: Generally lead in innovation-driven sectors such as technology, artificial intelligence, biotech and clean energy. US markets tend to introduce thematic ETFs earlier and with larger scale.

- European UCITS ETFs: Increasingly focus on themes tied to EU policy priorities, including sustainability, the green transition, defence and digitalisation. According to AXA IM, thematic and active UCITS ETFs saw record inflows in 2024 and 2025, reflecting Europe’s broader regulatory direction toward sustainable and digital economic growth.

Example Comparison: US vs UCITS MSCI World ETFs

| Factor | US MSCI World ETF | UCITS MSCI World ETF (e.g., IWDA, VWCE) |

|---|---|---|

| Index Coverage | ~1,500 global stocks | ~1,500 global stocks |

| Currency | USD | EUR / GBP / USD share classes |

| TER | ~0.12% | ~0.20% |

| Historical Return (2015–24) | ~9% p.a. (USD) | ~8.7% p.a. (EUR) |

| Accessibility (EU retail) | Restricted (PRIIPs) | Broad EU availability |

Performance differences between global US ETFs and UCITS equivalents are typically small; for European investors, currency risk is the factor that most often determines the gap.

UCITS vs Global ETFs: Pros, Cons, and Investor Profiles

After examining costs, regulation, taxation, liquidity and performance, the central question remains: which type of ETF should European investors choose — global US-domiciled ETFs or European UCITS ETFs? Experience shows that your own investor profile, risk tolerance and long-term strategy matter far more than headline TER differences.

Pros and Cons Summary

| Aspect | US-Domiciled ETFs (Global) | UCITS ETFs (Europe) |

|---|---|---|

| Costs (TERs) | Very low (0.03–0.07%) | Low but slightly higher (0.07–0.20%) |

| Accessibility | Limited due to PRIIPs; retail investors typically blocked | Fully available via EU brokers |

| Taxation | 30% withholding (15% with treaty), estate-tax risk | 15% withholding at fund level, no estate tax |

| Liquidity | Extremely high; tight spreads | High for large funds, wider for niche ETFs |

| Currency | USD-denominated; FX risk for EU investors | EUR/GBP share classes; hedged options available |

| Regulation | SEC oversight; strong governance | UCITS framework + PRIIPs + MiFIR investor protections |

| Thematic Choice | Broader innovation; faster product launches | Strong growth in ESG and EU policy-linked themes |

“For the vast majority of European retail investors, UCITS ETFs remain the only practical and tax-efficient choice.”

Investor Profiles

Passive Long-Term Investor in Europe

Best fit: UCITS ETFs

Why: Tax-efficient, easy to access, minimal administrative burden and EUR-denominated share classes that reduce currency volatility.

Cross-Border or Professional Investor

Best fit: US-domiciled global ETFs

Why: Lower TERs, exceptional liquidity and access to the full US product shelf. Requires treaty awareness and typically a professional-investor setup due to PRIIPs restrictions.

Dividend-Focused Investor

Best fit: UCITS ETFs domiciled in Ireland or Luxembourg

Why: Treaty benefits are handled automatically at fund level, avoiding 30 percent US withholding tax and eliminating estate-tax exposure entirely.

Thematic or Sector Investor

Best fit: Depends on the theme

Why: US ETFs lead in technology and innovation-heavy sectors, while UCITS ETFs increasingly capture ESG, sustainability and EU policy-driven themes. Demand for these European strategies has surged in recent years.

The Retail vs Professional Divide

According to PwC’s European ETF Market 2024, more than 80 percent of European ETF inflows went into UCITS funds, underscoring their dominance among retail investors. While US ETFs remain attractive to institutions and sophisticated investors for their ultra-low fees and deep liquidity, for roughly 95 percent of European retail investors UCITS ETFs are the most practical, accessible and tax-efficient option.

This divide is unlikely to change soon, making UCITS ETFs the enduring default for most European households.

Conclusion

Choosing between Global vs European ETFs is ultimately less about the index itself and far more about what matters to European investors in practice: costs after tax, regulatory protection, currency risk and day-to-day accessibility. While US-domiciled ETFs offer razor-thin TERs and exceptional liquidity, experience shows that these advantages often fade once withholding taxes, estate-tax exposure, FX costs and PRIIPs restrictions are taken into account.

UCITS ETFs, by contrast, are built specifically for European investors. They provide strong investor protection under the UCITS and PRIIPs frameworks, automatic tax treaty benefits at the fund level, EUR-denominated share classes, broad broker availability and a rapidly expanding range of thematic and ESG-aligned strategies. This is why the vast majority of ETF inflows in Europe continue to flow into UCITS structures — and why they remain the natural starting point for most long-term retail investors in the EU and UK.

For professional or cross-border investors with access to US products, global ETFs can still play a role — particularly for those who prioritise ultra-low fees and deep liquidity. But for everyday investors building long-term wealth in Europe, UCITS ETFs remain the most practical, efficient and accessible option.

If you want a practical example of how European investors combine global and UCITS ETFs in a simple allocation, see

How to Build a €1000 ETF Portfolio in Europe

Key Takeaways

- UCITS ETFs are designed for European investors, offering cleaner taxation, stronger regulation and full accessibility across EU brokers.

- US ETFs may have lower TERs, but FX costs, withholding tax and estate-tax exposure often outweigh this advantage for Europeans.

- Currency risk is the key driver of performance differences, not fund domicile or replication method.

- Liquidity is more than sufficient in large UCITS ETFs, despite lower volumes than their US counterparts.

- Retail investors overwhelmingly favour UCITS, while US ETFs remain most relevant for professionals.

- The choice depends on investor profile, but for around 95% of European retail investors, UCITS ETFs remain the most practical long-term solution.

FAQ

Can European retail investors buy US-domiciled ETFs like VOO or QQQ?

In most cases, no. Due to PRIIPs rules, US ETFs that do not publish a Key Information Document (KID) are blocked for European retail investors. Access is generally limited to professional and certain cross-border accounts.

Are UCITS ETFs safer than US ETFs?

Not safer in performance terms, but safer in structure for Europeans. UCITS funds follow strict diversification rules, asset-segregation requirements and investor-protection standards that are fully aligned with EU regulation.

Why do UCITS ETFs have slightly higher TERs than US ETFs?

UCITS funds comply with additional EU regulations and distribution requirements, which add administrative costs. Even so, the overall cost difference is usually offset by lower FX friction and better tax treatment for European investors.

Do UCITS ETFs give the same diversification as US ETFs?

Yes. UCITS ETFs tracking global indices such as MSCI World or FTSE All-World provide essentially identical diversification to their US counterparts. The main difference lies in currency denomination, not coverage.

How does currency risk affect returns for European investors?

US-denominated ETFs expose Europeans to EUR/USD movements. In years when the euro weakens, returns can rise; when it strengthens, returns fall. EUR-denominated or hedged UCITS share classes help reduce this volatility.

What about dividend taxes? Are UCITS really more efficient?

For most Europeans, yes. UCITS ETFs domiciled in Ireland or Luxembourg apply the US–Ireland tax treaty at the fund level, reducing withholding from 30% to 15% automatically. With US ETFs, investors must file forms themselves and still face estate-tax risk.

Are US ETFs always better for liquidity?

US ETFs have deeper liquidity and tighter spreads, but for most European investors the difference is marginal. Large UCITS ETFs typically offer spreads tight enough for efficient trading during European market hours.

Who should consider US-domiciled ETFs?

Primarily professionals, cross-border investors and those with access to non-retail platforms. These investors can benefit from lower TERs, full product access and treaty management — provided they understand the tax implications.

Do UCITS ETFs offer good thematic and sector options?

Yes. Thematic UCITS ETFs have expanded significantly, especially in ESG, green transition, digitalisation and defence themes aligned with EU policy. While the US still leads in tech-focused innovation products, Europe is catching up quickly.

Which type of ETF is best for long-term investors in Europe?

For around 95% of European retail investors, UCITS ETFs are the most practical and tax-efficient choice. They offer broad diversification, clean taxation, EUR share classes and full regulatory protection under the UCITS framework.

Matias Buće has a formal background in administrative law and more than ten years of experience studying global markets, forex trading, and personal finance. His legal training shapes his approach to investing — with a focus on regulation, structure, and risk management. At Finorum, he writes about a broad range of financial topics, from European ETFs to practical personal finance strategies for everyday investors.

Sources & References

EU regulations & taxation

- Bankeronwheels.com — Banker on Wheels

- Bny.com — 30% withholding tax

- Bvi.de — estate-tax uncertainty entirely

- European Commission / Taxation & Customs — Exchange-traded funds (ETFs)

- investor protections

- Markets in Financial Instruments Regulation (MiFIR)

- MiFIR

- no single issuer may exceed 10% of the fund

- PRIIPs regulation

- US ETFs

- Irs.gov — $60,000 in US-situs assets

- US estate tax

- KPMG

- Pwc.lu — PwC

- PwC Tax Summaries — PwC

Additional educational resources

- Axa-im.com — AXA IM

- AXA IM

- Bajajamc.com — Bajaj AMC

- Blackrock.com — S&P 500 ETF

- Efama.org — UCITS Directive

- Etftrends.com — ETFtrends

- Irs.gov — 15% with treaty & W-8BEN

- US assets

- Ishares.com — iShares Core S&P 500 UCITS ETF (CSPX)

- justETF

- justETF

- Morningstar

- Msci.com — MSCI World

- Oliverwyman.com — Oliver Wyman

- Ssga.com — SPDR S&P 500 ETF (SPY)