Europe in 2026 is a very different place to invest than just 5 years ago. Falling fees, stricter regulations, and new fintech apps made it possible to build a diversified portfolio with as little as €1,000.

Disclaimer:

The information provided on Finorum is for educational and informational purposes only and does not constitute financial, investment, or tax advice.

Investing involves risk, including the potential loss of capital.

Always conduct your own research or consult a qualified financial advisor before making investment decisions.

Finorum does not promote or endorse any specific financial products or institutions.

Investing €1,000 in Europe in 2026 is a smart and realistic way to start building wealth.

Focus on low-cost UCITS ETFs (around 70%), complement with bonds or savings (20%), and keep a small share (10%) for learning or higher-risk assets like crypto or crowdfunding.

Before investing, make sure you have an emergency fund, no high-interest debt, and basic insurance — stability first, growth second.

Why Starting With 1000 Euros Matters for Investing in Europe

Small Beginnings, Big Lessons

Starting your investment journey with €1,000 might sound humble, almost too small to make a difference. But in reality, it’s one of the most practical and realistic entry points into the world of investing — especially for beginners across Europe who want to learn without taking on too much risk.

As both Moneyfarm and justETF beginner guides highlight, €1,000 is already enough to build a compact, diversified mini-portfolio across several asset classes — from ETFs and bonds to savings products or even fractional real estate. It’s not about how much you start with, but about starting right.

If you want to know more about the core building blocks for beginners in Europe, start with

Best UCITS ETFs in Europe (2026)

Best Brokers in Europe for Beginners (2026)

Why €1,000 Is the Sweet Spot for New Investors

There are several reasons why this amount — modest, but meaningful — is often seen as the “sweet spot” for getting started:

- Diversification without overexposure. With €1,000, you can split your investment across two or three asset classes — for instance, 70% ETFs, 20% bonds, and 10% savings or crypto — without falling into the trap of overconcentration. You get exposure to multiple types of returns while keeping your risk manageable.

- Psychological comfort. It’s a sum that matters, but it won’t keep you awake at night. Behavioural finance studies, such as those discussed by Investopedia (2025), show that starting small helps new investors overcome the fear of losing money. You build consistency and confidence step by step — habits that often matter more than the first return.

- Low barriers to entry. The new wave of European investing platforms like Trade Republic and Scalable Capital make it easier than ever to get started. With minimum investments as low as €1, you no longer need to wait years to build up capital. A thousand euros is already plenty to open an account, diversify, and begin learning by doing.

- Learning through experience. Putting €1,000 to work gives you real, hands-on experience. You’ll see how markets move, how fees and taxes apply, and how your emotions respond to volatility — all before you commit larger amounts. Think of it as your “investment apprenticeship”: the phase where you’re building skills, not just wealth.

If you want to see how €1,000 can actually be allocated in practice:

How to Build a €1000 ETF Portfolio in Europe

The Power of Compounding — What €1,000 Can Become

To put things into perspective: if you invested €1,000 in a low-cost UCITS ETF with an average annual return of about 7% — roughly the long-term historical equity market average, according to Morningstar (2025) — your initial investment could grow to nearly €3,870 in 20 years. That’s almost four times your starting amount, without adding a single extra euro.

This is the quiet magic of compounding — where time does most of the heavy lifting. The earlier you start, the longer your money works for you.

If you want to know more:

S&P 500 UCITS vs Euro Stoxx 50: A Comparison for 2026

Reframing How You See Money

Think about it this way: €1,000 is roughly what many Europeans spend on a two-week summer holiday, or what slips away over a year of streaming and app subscriptions. Redirecting that same sum into an ETF, bond, or savings plan could be the first step toward long-term financial independence.

According to Investopedia, one of the most powerful mental shifts a new investor can make is reframing spending money as investment capital. When you stop thinking of money as something to burn and start seeing it as a tool to grow, everything about your financial habits changes.

The Real Value of Investing €1,000

If you’re wondering how to invest 1,000 euros in Europe, remember — this isn’t just about chasing returns or timing the perfect market entry. It’s about participation. It’s about getting your hands dirty with real experience in Europe’s financial ecosystem — learning how fees work, understanding taxes and regulations, and building the kind of discipline that leads to sustainable wealth over time.

Your first €1,000 is more than capital — it’s your first investment in yourself.

Check Your Financial Health Before Investing 1,000 Euros in Europe

Before You Invest, Step Back and Assess

Before putting your first €1,000 to work, take a breath and look at the bigger picture — your overall financial health. Investing isn’t just about choosing the right ETF or fund; it’s about being in a position to invest safely and sustainably. As highlighted by Moneyfarm (2025) and Curvo, it’s important to build financial stability before chasing returns.

Think of it like building a house. You wouldn’t start decorating before laying a solid foundation. The same goes for investing: if your financial base — savings, controlled debt, and proper insurance — isn’t solid, even the best investment choices can collapse under pressure.

If you want to know more:

Low-Fee vs High-Fee Brokers in Europe

Build an Emergency Fund First

Before you invest a single euro, make sure you have an emergency cushion. Most financial institutions, including the European Banking Authority (EBA), recommend setting aside three to six months of essential living expenses in a safe, easily accessible account such as a savings or money market fund.

Across Europe, the average household spends between €1,200 and €2,000 per month, meaning a healthy safety net typically falls somewhere between €4,000 and €10,000. If you haven’t reached that point yet, your first €1,000 can become the seed of your emergency fund — a simple but powerful start.

For example, in Scandinavia, where living costs are among the highest in Europe, households often aim for €10,000 or more in reserves. By contrast, in parts of Eastern Europe, €1,000 may already cover a full month of basic expenses — a meaningful cushion in case of job loss, illness, or a sudden bill.

Why does this matter? Because a proper emergency fund protects you from being forced to sell your investments when markets are down or from taking on expensive new debt when life throws surprises your way.

Clear High-Interest Debt Before Investing

One of the smartest things you can do before investing is to pay off high-interest debt. According to the European Central Bank (ECB), average credit card and consumer loan rates across the EU range between 6% and 10%, and in parts of Southern Europe, they can climb past 12%.

Compare that to the long-term average return of about 7% per year on diversified UCITS ETFs (as reported by Morningstar, 2025). It’s clear: paying down high-interest debt gives you a guaranteed return that no market can promise.

Take Markus, a 45-year-old professional from Germany. Instead of investing right away, he uses his €1,000 to pay off part of a credit card balance charging 9% interest. That single decision saves him roughly €90 a year in interest — more than the €70 he might earn from an ETF in the same period, and without any risk or volatility.

Source: ECB Data Portal — “Consumer credit” dataset, European Central Bank

In short, eliminating high-interest debt is often the most reliable “investment” you can make with €1,000. It strengthens your financial stability, reduces stress, and gives you the breathing room to start investing confidently later on.

Protect Your Income and Stability

Even in Europe — a region known for relatively strong social safety nets — not every risk is covered. Dental care, private healthcare, or temporary loss of income often fall outside state protection. Setting aside part of your budget for basic insurance coverage (whether health, life, or income protection) can prevent you from having to sell investments early to cover emergencies.

Insurance might not give you visible “returns,” but it provides something just as valuable — continuity. Protecting your ability to earn ensures your financial plan stays on track even when life doesn’t go according to plan.

Build Stability Before You Grow

Many beginners see €1,000 as the starting line for their investing journey. In reality, the smarter first step is to use that same €1,000 to strengthen your financial foundation — by topping up your emergency fund, paying off debt, or arranging essential insurance.

These actions don’t just make you safer; they make you more investable. Once you’re stable, every euro you invest will work harder because it won’t be pulled back by interest payments, emergencies, or instability. Financial resilience is the hidden side of wealth building — it’s what separates those who stay invested from those who are forced out by circumstance.

A Quick Self-Check Before You Invest

Before you move forward and learn how to invest 1,000 euros in Europe, ask yourself three simple but powerful questions:

- Do I have at least three months of expenses saved?

- Am I free from high-interest debt like credit cards or consumer loans?

- Do I have basic insurance coverage in place?

If you can confidently answer “yes” to all three, you’re ready to begin investing your first €1,000. If not, that’s perfectly fine — focus on those foundations first. They’re the most reliable return on investment you’ll ever get.

Beyond the Basics — Setting Your Investment Foundation

Once your finances are stable, the real journey begins. Even with €1,000, clarity of purpose matters more than the amount itself.

Start by defining your goals and time horizon. Are you saving for something within five years, like a house deposit, or are you investing long-term, perhaps for retirement?

Example: Anna, a 28-year-old from Spain, has no debt and a stable job. She invests her €1,000 into a global UCITS ETF, focusing on gradual growth over 20 years rather than short-term profits.

Next, consider liquidity. Some European products — like SCPI real-estate funds or certain insurance-linked investments — can tie up your money for years. If you expect to need access sooner, choose more liquid options such as ETFs or savings plans.

Be mindful of currency risk too. If you earn or hold savings in GBP, PLN, or CHF, or invest outside the eurozone, exchange-rate movements can affect your returns — sometimes positively, sometimes not.

Finally, commit to continuous learning. The most successful investors are students of the market. Stay informed about MiFID II, PRIIPs, and other EU investment frameworks. Follow reliable sources like PwC Tax Summaries, KPMG EU Tax Centre, and ESMA for updates on regulations and taxation.

And remember: even with a small amount, diversification matters. Dividing €1,000 across two or three asset classes — for instance, 70% ETFs, 20% bonds, and 10% savings or crypto — can make your portfolio more balanced and personal.

If you want to know more:

Why US ETFs Are Restricted in Europe (PRIIPs Rules Explained)

The Most Common Ways to Invest 1,000 Euros in Europe

From Saving to Investing — Where to Begin

Once your financial foundation is solid, the next step is figuring out how to invest 1,000 euros in Europe as a beginner. And here’s the good news: European investors in 2026 have access to more options than ever before. Whether you’re looking for the safety of savings products, the steady returns of bonds, the growth potential of ETFs, or something more adventurous like real estate crowdfunding or crypto — there’s a path that fits your goals and comfort level.

Each type of investment comes with its own mix of returns, risk, and liquidity. Understanding these differences early on will help you make smarter, calmer decisions — even with a relatively small amount of money.

Best Investments for Beginners in Europe (2026)

Here’s a quick comparison of the most common ways Europeans invest small amounts like €1,000:

| Investment Option | Average Annual Return (2025 est.) | Risk Level | Liquidity | Notes (Europe-specific) |

|---|---|---|---|---|

| Savings account / Term deposit | 1–3% | Very low | High | Secure, but inflation often outpaces returns. In some EU countries still below 2%. |

| Government bonds (Eurozone) | 2–4% | Low | Medium | Safe and predictable, though yields are higher in Southern Europe than in Germany or France. |

| Corporate bonds | 3–5% | Low–Medium | Medium | Better returns than gov. bonds, but credit quality matters. |

| ETFs (UCITS, equity index) | 6–8% | Medium | High | The most popular choice for beginners — diversified, low-cost, and euro-friendly under UCITS regulation. |

| Individual stocks | Variable (0–15%+) | Medium–High | High | High potential returns but higher risk and requires research and discipline. |

| SCPI / REIT (fractional real estate) | 4–6% | Medium | Low | Popular in France & Germany. Offers steady yields but locks funds for several years. |

| Real estate crowdfunding | 7–10% | Medium–High | Low | Platforms like Profitus allow entry from €100. Higher yield, but project risk exists. |

| Peer-to-peer lending (P2P) | 7–12% | High | Low–Medium | Platforms like Lendermarket offer strong returns, but depend on borrower repayments. |

| Cryptocurrencies | Highly volatile (–50% to +200%) | Very High | High | Best kept to a small allocation. EU’s MiCA (2024) framework adds regulation, but volatility remains. |

Why Liquidity Matters More Than You Think

A lot of beginners focus only on returns — but liquidity (how easily you can access your money) can make or break your experience. While ETFs or savings accounts can be cashed out within days, SCPI or crowdfunding projects might lock your funds for years. If you think you’ll need quick access to cash, choose flexible investments.

Anna, Markus and Elisabeth: Three Different Approaches

To make it real, let’s look at three different beginner investors in Europe — each starting with the same €1,000, but with very different priorities.

- Anna (28, Spain) → A young professional with no debt and long-term goals. She invests €800 into a global UCITS ETF, €150 into government bonds, and €50 in a savings account. Her focus is on long-term compounding — letting time and consistency do the heavy lifting.

- Markus (45, Germany) → Mid-career, more cautious after paying off debt. He divides €500 into ETFs, €300 into SCPI real estate, and €200 into peer-to-peer lending to generate a little extra income.

- Elisabeth (65, Austria) → Retired, focused on stability and income. She puts €600 into corporate bonds, €300 into REITs, and €100 into a dividend ETF for modest growth.

Each of them uses €1,000 differently, based on age, goals, and risk tolerance. That’s the essence of smart investing — matching your money to your life, not someone else’s strategy.

If you want to know more:

Best UCITS ETFs in Europe (2026)

Taxes and Accessibility — Two Things You Can’t Ignore

When it comes to investing in Europe, taxes and accessibility often matter as much as the investment itself.

Taxes: In most EU countries, capital gains and dividends are taxable, but the rates vary dramatically. For example, Ireland taxes capital gains at 33%, while Germany applies a flat 25% Abgeltungsteuer. That means the same ETF can generate different net returns depending on where you live. (For more on this, check our upcoming guide on dividend taxes in Europe.)

Accessibility: Not every investment is available everywhere. For instance, SCPI real estate products are common in France but harder to access in Central and Eastern Europe. Meanwhile, many large P2P lending platforms are Baltic-based — accessible to EU investors, but not always passported to every country. Always check what’s available in your jurisdiction before committing funds.

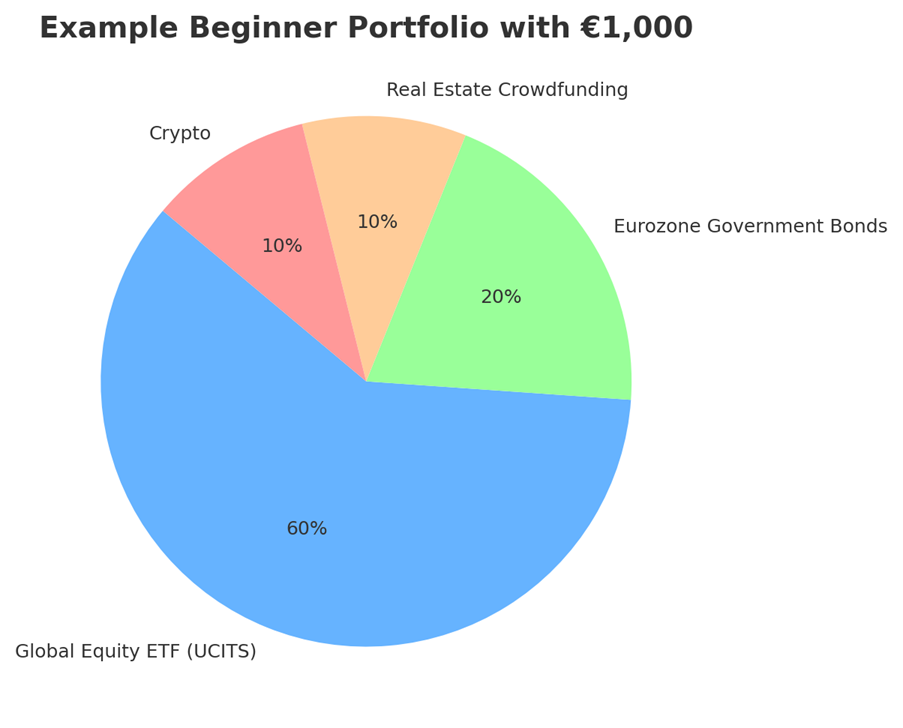

Example Beginner Portfolio — Diversification in Action

Here’s how a balanced portfolio with €1,000 might look for a first-time investor in Europe:

€100 (10%) → Crypto (Bitcoin or Ethereum): High-risk, small exposure to learn and explore digital assets.

€600 (60%) → Global equity ETF (UCITS): Core long-term growth and diversification across global markets.

€200 (20%) → Eurozone government bonds: A stabilising layer of safety and predictable returns.

€100 (10%) → Real estate crowdfunding (Profitus-type project): Adds alternative income and experience in property-backed assets.

If you’re unsure whether to focus on global or local exposure as a European investor

Global vs European ETFs: Which Is Better for Investors?

A Simple Tip for New European Investors

Even with limited capital, diversification is absolutely possible. A general rule: keep 70–80% of your portfolio in “core” assets like ETFs and bonds, and use the remaining 20–30% as “learning capital” — experimenting with crowdfunding, crypto, or niche projects.

This approach balances growth with education. You’ll not only grow your savings but also gain first-hand experience — learning how European markets, platforms, and regulations truly work.

How to Choose the Right Broker in Europe (2026)

Why Your Choice of Broker Matters

No matter where you plan to invest your €1,000 — ETFs, bonds, real estate, or even crypto — you’ll need a broker or investing app to get started. Choosing the right platform is one of the most important decisions for beginners, because fees, usability, and regulation directly affect your long-term returns.

In 2026, European investors have more choice than ever. From traditional full-service brokers to app-based platforms like Trade Republic and Scalable Capital, the landscape has become more competitive — and more confusing. Knowing what to look for will help you save money, avoid frustration, and stay safe.

Regulation and Investor Protection

One of the biggest advantages of investing in Europe is strong investor protection. All legitimate European brokers and trading apps operate under strict EU-wide and national regulations:

- MiFID II (Markets in Financial Instruments Directive) and the European Securities and Markets Authority (ESMA) ensure transparency, fair pricing, and minimum investor protections.

- National regulators such as BaFin (Germany), AMF (France), and CNMV (Spain) enforce local compliance and monitor licensed entities.

- Many brokers also participate in Investor Compensation Schemes, which protect retail investors up to €20,000 under EU law — and even more in certain countries (for example, up to €100,000 in Germany for cash deposits).

Bottom line: Always choose a fully EU-regulated broker that clearly lists its investor compensation scheme and regulatory oversight. If the platform hides this information, that’s a red flag.

Best Brokers in Europe for 2026

Here’s a quick comparison of popular, trusted platforms often recommended for beginners investing small amounts like €1,000:

| Broker / Platform | Fees & Commissions | Minimum Deposit | Best For | Notes (Europe-specific) |

|---|---|---|---|---|

| DEGIRO | Low trading fees (ETFs often €0) | €0 | ETF & stock investors | Widely available in EU, regulated by Dutch AFM. |

| Trade Republic | €1 per trade | €1 | Beginners & mobile investors | German broker, app-first, offers ETF savings plans (Sparpläne). |

| Interactive Brokers (IBKR) | Very low global fees | €100 | Advanced users & global markets | EU clients under Irish regulator (CBI). |

| Scalable Capital | €0–2.99 monthly plans | €1 | ETF savings plans | Strong in Germany & Austria. |

| eToro | Commission-free stocks & ETFs | €50 | Social trading & beginners | CySEC-regulated, multi-asset exposure. |

| Revolut / N26 Invest | Commission-free up to limit | €1 | Micro-investments | Banking apps with light investing features. |

Many beginners fixate on trading fees, but those are just part of the story. Custody charges, FX mark-ups and even inactivity fees can eat into your returns far more than a €1 commission. The platform that looks “free” at first glance often isn’t once you do the math.

If you want to know more:

Best Brokers in Europe for Beginners (2026)

What to Look for When Comparing Brokers

When choosing where to open your first investing account, take a step back and evaluate more than just fees. The right platform should feel intuitive, transparent, and trustworthy.

Here’s what to pay attention to:

- Fees: Even a 1% trading cost can eat into long-term returns.

- Ease of use: A clean, simple app helps beginners avoid costly mistakes.

- Range of products: Does the broker offer only ETFs, or also crypto, P2P, and funds?

- Regulation: Always confirm EU + national regulator oversight.

- Deposits & withdrawals: Check minimums and SEPA transfer availability.

- Language & support: Local-language service can make a big difference.

- Withdrawal rules: Look for any hidden costs or long delays.

How Different Investors Choose Their Broker

To show how personal this decision can be, let’s revisit our three fictional investors:

- Anna (28, Spain) → Wants low-cost automation. She opens an account with Trade Republic, sets up an ETF savings plan, and automates €100 monthly contributions.

- Markus (45, Germany) → Prefers a wider range of ETFs and bonds. He chooses DEGIRO for its low fees and strong desktop tools.

- Elisabeth (65, Austria) → Values simplicity and security. She invests through her bank’s app (N26 Invest), accepting slightly higher costs for convenience and peace of mind.

Each of them made a different choice — and that’s perfectly fine. The right broker depends on how you invest, not just what you invest in.

Step-by-Step — How to Open a Broker Account in Europe (2026)

Getting started is easier than ever. Here’s how most European investing platforms work, step by step:

Compare platforms – Look at fees, supported markets, and usability.

Check regulation – Verify EU + local regulator (e.g., BaFin, AMF, CNMV) and investor compensation coverage.

Prepare documents – You’ll need your passport or ID, proof of address, and tax ID.

Complete KYC – Most brokers require an online identity check and a short questionnaire about your investing experience and risk tolerance.

Fund your account – Use a SEPA transfer or card payment. Be mindful of currency-conversion fees.

Place your first order – Search your chosen ETF by ticker or ISIN, review its factsheet, and understand whether it’s accumulating (Acc) or distributing (Dist).

Automate & secure – Set up an ETF savings plan (DCA), enable two-factor authentication, and keep your tax reports safe.

Many first-time investors focus on €1 trading fees, but that’s rarely the whole story. Always check what you’ll pay in FX, custody, or inactivity charges — it’s the total cost that decides whether your broker is truly good value.

If you want to know more:

How to Open a Brokerage Account in Europe (Step by Step)

Taxes and Regulations in Europe

Disclaimer:

The information in this section is provided for educational and informational purposes only and does not constitute legal, tax, or investment advice.

Tax rules vary by country and may change over time. Always verify the latest regulations with a certified tax advisor or your local tax authority before making any investment or reporting decisions.

Finorum does not take responsibility for any actions taken based on this information.

Why Taxes Can Make or Break Your Investment Returns

Even the smartest investment plan can fall flat if you ignore one crucial factor — taxes. In Europe, the same ETF, bond, or real estate product can yield entirely different results depending on where you live. That’s why understanding taxation is just as important as choosing your investments.

According to PwC Tax Summaries (2025) and the KPMG EU Tax Centre, capital gains and dividend taxes vary widely across EU member states. The difference can be striking: an investor in Germany and one in Spain can hold the same fund but end up with very different net returns simply because of local tax rates.

In other words, when you invest 1,000 euros in Europe, your after-tax outcome depends not just on what you buy — but where you buy it.

Capital Gains and Dividend Taxes in Europe (2026 Overview)

Here’s a simplified comparison of how major EU countries tax investment income:

| Country | Capital Gains Tax (CGT) | Dividend Tax | Notes |

|---|---|---|---|

| Germany | 25% flat (Abgeltungsteuer) | 25% | Banks and brokers usually withhold tax automatically. |

| France | 30% flat (Prélèvement Forfaitaire Unique) | 30% | Single “flat tax” rate covering both capital gains and dividends. |

| Spain | 19–28% progressive | 19–28% progressive | Rates rise with income. |

| Italy | 26% flat | 26% | Equal rate for both CGT and dividends. |

| Ireland | 33% flat | 25% | One of the highest CGT rates in Europe. |

| Belgium | 10% (from 2026) | 30% | Major tax reform under way — CGT introduced for the first time. |

Note: In many EU countries, brokers automatically deduct dividend taxes at the source — a process called withholding tax. For cross-border investors, this can sometimes lead to double taxation, unless a tax treaty between your home country and the fund’s domicile applies.

For more detail, see the PwC Dividend Tax Rates in Europe and the KPMG EU Tax Centre — both excellent resources for comparing how tax policy differs across borders.

Why It Matters for Everyday Investors

Taxes don’t just affect wealthy investors — they matter to anyone putting their first €1,000 into the market. Here’s how three of our earlier examples approach it:

- Anna (Spain): invests mainly in ETFs. Because Spain taxes long-term gains progressively, she also contributes to pension-style products for better tax treatment over time.

- Markus (Germany): knows his 25% flat tax will hit every dividend, so he prefers accumulating (Acc) ETFs that reinvest payouts and postpone taxation.

- Elisabeth (Austria): focuses on stability through bonds and REITs, accepting her 27.5% income tax rate — because for her, reliability matters more than squeezing out extra after-tax returns.

Their examples show how the same €1,000 investment can produce very different results after tax, depending on your location, asset type, and use of tax-advantaged accounts (like Germany’s Freistellungsauftrag, France’s PEA, or UK ISAs).

Three Practical Ways to Reduce Tax Drag in Europe

European investors have several legitimate ways to minimise the tax drag on their investments — small adjustments that can make a big difference over time.

1. Use Accumulating (Acc) ETFs

Instead of paying out dividends, these funds automatically reinvest income back into the portfolio. This not only boosts compounding but also defers taxation, allowing your gains to grow before the tax bill arrives.

2. Choose Treaty-Optimised Domiciles

Funds domiciled in Ireland or Luxembourg — especially UCITS ETFs — often benefit from stronger double-tax treaties. That means lower withholding tax on foreign dividends compared to domestic funds. Over years, that can add up to meaningful extra returns.

3. Invest Through Local Tax Wrappers

Take advantage of country-specific tax shelters designed for long-term investors:

- Germany → Freistellungsauftrag: tax-free allowance up to €1,000 per year.

- France → PEA (Plan d’Épargne en Actions): tax benefits after 5 years of holding.

- UK → ISA (Individual Savings Account): complete exemption on growth and income.

Using these wrappers is one of the simplest and most effective ways to keep more of your returns — especially for those starting small.

Why Tax Planning Is Part of Smart Investing

The same ETF can perform very differently depending on how you structure it — whether you pick Acc vs. Dist share classes, use an Irish-domiciled UCITS fund, or invest through a tax wrapper. Understanding these nuances isn’t about avoiding tax; it’s about being efficient and keeping your hard-earned returns where they belong — working for you.

In short, learning the tax side of investing is one of the most underrated skills in Europe’s investment landscape. Smart investors don’t just chase returns — they plan for what happens after the return.

Example Portfolios for 1,000 Euros

From Theory to Practice — Building Your First European Portfolio

Knowing the theory is useful — but seeing how it works in practice is even better. Let’s explore how a beginner could actually invest €1,000 in Europe in 2026. The idea is simple: balance risk, return, and liquidity depending on your goals and comfort level.

According to Morningstar (2025) and justETF beginner research, even a small investment can be well-diversified if you focus on the right building blocks — combining UCITS ETFs, bonds, cash, and alternatives like crowdfunding or crypto.

Conservative Portfolio — Stability First

| Allocation | Amount (€) | Description |

|---|---|---|

| Eurozone government bonds | 500 (50%) | Reliable, low-risk income source |

| High-interest savings account / term deposit | 300 (30%) | Flexible and stable buffer |

| Dividend-paying UCITS ETF | 200 (20%) | Adds moderate growth and yield |

This portfolio suits retirees or cautious investors like Elisabeth (65, Austria) — people who prioritise stability over high returns. The focus is on capital preservation and consistent income, not chasing the market.

According to the European Central Bank (ECB), average Eurozone government bond yields in 2025 ranged between 2–4%, providing modest but predictable returns. It’s the kind of setup that helps you sleep well at night, even when markets get noisy.

Balanced Portfolio — Growth Meets Stability

| Allocation | Amount (€) | Description |

|---|---|---|

| Global UCITS ETF | 600 (60%) | Broad market exposure and growth |

| Eurozone corporate bonds | 200 (20%) | Steady income and diversification |

| Real estate crowdfunding (e.g., Profitus) | 100 (10%) | Alternative income potential |

| Cash savings | 100 (10%) | Flexibility for opportunities |

This mix fits investors like Markus (45, Germany) — someone who values both growth and resilience. It’s the “best of both worlds” approach: enough equity exposure for compounding returns, balanced by safer assets that buffer against volatility.

According to the Investingintheweb Broker Report (2025), this blend of ETFs and euro-denominated bonds is one of the most popular portfolio setups among German retail investors, thanks to its simplicity and balanced profile.

Growth Portfolio — Playing the Long Game

| Allocation | Amount (€) | Description |

|---|---|---|

| Global UCITS ETF (equities) | 800 (80%) | Long-term compounding driver |

| Emerging markets ETF or small-cap stocks | 100 (10%) | High-growth potential, higher risk |

| Crypto (BTC or ETH) | 50 (5%) | Experimental, volatile, long-term upside |

| P2P lending (e.g., Lendermarket) | 50 (5%) | Alternative income source |

This setup is perfect for investors like Anna (28, Spain), who have time on their side and can handle some short-term swings for the chance of higher long-term returns.

Her focus is compounding growth over decades, not short-term wins. Under the MiCA regulation (2024), European crypto platforms face tighter controls and higher transparency standards, making small experimental allocations safer — but still highly volatile.

Portfolio Comparison at a Glance

| Portfolio Type | Focus | Expected Return (p.a.) | Risk Level | Liquidity |

|---|---|---|---|---|

| Conservative | Capital preservation, income | 2–4% | Low | High (bonds/savings) |

| Balanced | Growth + stability | 4–6% | Medium | Medium–High |

| Growth | Long-term compounding | 6–9% (volatile) | High | Medium–High |

Most beginners in Europe start with a balanced portfolio. It offers the comfort of stability while still giving your money a chance to grow. Over time, all three approaches can be scaled easily using monthly savings plans, adding structure and discipline to your investing routine.

The Rise of Savings Plans and Small Investors in the EU

In countries like Germany and Austria, brokers such as Trade Republic and Scalable Capital now offer ETF savings plans (Sparpläne) starting from as little as €25 per month.

That means your initial €1,000 doesn’t just sit there — it can become the foundation for a long-term wealth habit. You start small, contribute monthly, and let time and compounding do the heavy lifting.

Modern Investment Trends Shaping Europe’s Markets

The European investment landscape is evolving fast — even for small investors.

- Sustainable Finance (ESG): The EU’s Sustainable Finance Disclosure Regulation (SFDR) and the EU Taxonomy are pushing for more transparent, sustainable investing. Even small portfolios can now include ESG-focused ETFs.

- Digitalisation of Finance: Thanks to ESMA and European Commission initiatives, onboarding is now fully digital — from SEPA transfers to automated reporting.

- ELTIFs (European Long-Term Investment Funds): Reformed in 2024, these funds now allow broader retail participation. They may not suit a €1,000 entry yet, but they’re a glimpse of the future for long-term European investors.

- Tax Evolution: National tax rules keep shifting. Following PwC Tax Summaries or KPMG EU Tax Centre can help beginners stay informed and compliant.

Simple Starting Point for Beginners

If you’re not sure where to begin, keep it simple:

80% in a global UCITS ETF + 20% in something safe, like bonds or a savings account.

This minimalist setup gives you global exposure, manageable risk, and flexibility. As you gain experience and confidence, you can start adding small positions in real estate crowdfunding, P2P lending, crypto, or ESG funds.

Common Mistakes Beginners Should Avoid

The Pitfalls Every New Investor Should Watch Out For

Even the most carefully built portfolio can stumble if you fall into the same traps that catch many first-time investors. According to the ESMA Retail Investor Report (2025) and OECD research on financial literacy, there are a few recurring mistakes European beginners make when they start investing their first €1,000 — and they’re surprisingly easy to avoid once you know what to look for.

1. Ignoring Fees and Hidden Costs

Fees are one of the silent killers of returns. Even a 1% annual fee can eat away more than 20% of your total gains over 20 years (Morningstar, 2025).

Many beginners focus only on trading commissions, but there’s often more hiding in the fine print — custody fees, FX conversion spreads, and withdrawal charges that quietly erode performance.

Markus, our mid-career investor from Germany, chose DEGIRO precisely because of its low ETF fees. Over time, that small decision saved him hundreds of euros — proof that a little homework goes a long way.

2. Putting Everything Into One Basket

Diversification isn’t a buzzword — it’s protection. Putting your full €1,000 into a single stock or cryptocurrency might feel bold, but it also means one bad week could wipe out months of savings.

Anna, the 28-year-old from Spain, avoided that by spreading her investments between ETFs, bonds, and a small crypto allocation. That balance gives her exposure to different markets without betting her entire future on one idea.

If you want to know more:

ETFs vs Crypto in Europe: What Investors Should Know (2026)

3. Chasing Quick Wins

The temptation to chase “hot tips” or time the market hits almost everyone at some point. Whether it’s a Reddit thread, a TikTok clip, or a Telegram group promising 50% gains, the result is usually the same — panic buying, panic selling, and disappointment.

Investing €1,000 in Europe should be about learning, compounding, and discipline — not gambling on headlines. The goal is to build financial habits that last decades, not chase a viral moment.

4. Forgetting About Liquidity

Not all investments are created equal when it comes to flexibility. Products like SCPI, ELTIFs, or real estate crowdfunding can offer solid returns but may lock your money for years.

Elisabeth, the 65-year-old from Austria, understands this well. She prefers liquid assets like bonds and ETFs that she can sell quickly if she needs cash. Always match your investments to your time horizon — flexibility matters just as much as returns.

5. Overlooking Taxes

Taxes can quietly change your results more than you think. The same UCITS ETF can deliver different net returns in Ireland versus Germany because of capital gains and dividend withholding taxes.

Beginners often forget that brokers automatically deduct these “withholding taxes” on foreign dividends, sometimes leading to double taxation unless a tax treaty applies.

If you’re not sure about your country’s rules, check PwC’s Dividend Tax Rates in Europe or the KPMG EU Tax Centre for up-to-date guidance.

6. Skipping Education and Ignoring Regulations

One of the most common beginner mistakes in Europe is diving into complex products without understanding the rules.

For instance, US-domiciled ETFs are off-limits for EU retail investors because of the PRIIPs regulation (ESMA, 2025) — yet many newcomers still waste hours trying to buy them. The solution? Start simple: UCITS ETFs, bonds, and regulated savings products. These instruments are designed to protect beginners while they learn.

Every experienced investor started small — not just with money, but with knowledge.

Smarter Habits That Make a Big Difference

Avoiding mistakes is half the battle. The other half is developing habits that keep you consistent:

- Stay disciplined. Emotional reactions — panic during dips, greed during rallies — are portfolio killers.

- Review periodically. Long-term investing doesn’t mean “set and forget.” Check your portfolio every 6–12 months and rebalance if needed.

- Set realistic expectations. Your first €1,000 won’t make you rich overnight. It’s the foundation for the skills and habits that will make you wealthy over time.

- Rely on trustworthy sources. Follow updates from ESMA, the European Commission (Taxation & Customs Union), and tax experts like PwC and KPMG instead of social media hype.

Quick Recap — Top 3 Mistakes to Steer Clear Of

| Mistake | Why It Matters |

|---|---|

| Paying high fees or ignoring hidden costs | Eats away long-term returns and compounds losses. |

| Putting all €1,000 into one asset | Leads to volatility and unnecessary risk. |

| Ignoring taxes and EU-specific regulations (like PRIIPs) | Reduces net returns and limits investment choices. |

The Real Goal Behind Your First €1,000

The goal of investing your first €1,000 in Europe isn’t to double it overnight — it’s to build investing habits, understand how markets behave, and avoid the classic beginner pitfalls.

Everyone makes mistakes at the start. The difference between those who grow and those who quit is simple: learn, adjust, and stay in the game.

Conclusion

Investing in Europe in 2026 isn’t just about finding the best ETF or timing the market — it’s about understanding how the pieces fit together. Whether you’re starting with €1,000 or building a larger portfolio, the principles stay the same: protect your foundation, diversify wisely, and keep an eye on costs, taxes, and regulation.

Europe’s financial landscape is evolving faster than ever — digitalisation, ESG, and new investment products are reshaping what’s possible for everyday investors. The key is to start small, stay consistent, and learn by doing. Every euro you invest becomes not just capital in the market, but experience that compounds over time.

Your first €1,000 is more than a number — it’s the beginning of a habit, a skill set, and ultimately, financial independence built step by step in one of the world’s most dynamic markets.

Key Takeaways

Stay consistent, stay curious — long-term investing success comes from patience, not prediction.

Even €1,000 is enough to start investing and build a diversified mini-portfolio in Europe.

Focus on low-cost, EU-regulated platforms and UCITS ETFs for transparency and safety.

Always review fees, taxes, and liquidity — they shape your real returns more than short-term market moves.

Strengthen your financial base first: emergency fund, no high-interest debt, and insurance.

FAQ

1. How can I start investing 1,000 euros in Europe as a beginner?

Start by choosing a regulated EU broker such as Trade Republic, DEGIRO, or Scalable Capital. Build a simple mix — for example, 70% in a global UCITS ETF, 20% in bonds, and 10% in savings or crypto. The goal isn’t the amount — it’s learning how investing works.

2. Is 1,000 euros enough to build a diversified portfolio?

Yes. Thanks to fractional investing and low-cost ETFs, €1,000 is enough to create a balanced mini-portfolio. Diversify across 2–3 asset classes, like ETFs, bonds, and savings, to spread risk.

3. What are the best investments in Europe for 2026?

The most popular investments among European beginners in 2026 are UCITS ETFs, government or corporate bonds, and ESG-focused funds. Real estate crowdfunding and P2P lending are growing alternatives, but they carry higher risk.

4. What’s the safest way to invest in Europe right now?

The safest options are Eurozone government bonds, savings accounts, and UCITS ETFs from large, regulated issuers like iShares or Vanguard. These offer stability, liquidity, and transparency under EU investor protection laws.

5. How are investments taxed in Europe?

Taxes vary by country. For example, Germany has a 25% flat tax on gains and dividends, France applies a 30% “flat tax”, and Spain uses progressive rates. Always check local rules or use tax wrappers like PEA (France) or Freistellungsauftrag (Germany) to reduce tax drag.

6. Which brokers are best for beginners in Europe?

Top options for 2026 include Trade Republic, Scalable Capital, and DEGIRO — all EU-regulated and beginner-friendly. For those who prefer mobile investing, Trade Republic and Scalable Capital stand out for simplicity and ETF savings plans.

7. What mistakes should I avoid when investing 1,000 euros?

Avoid chasing quick profits, ignoring fees, and putting all your money into one asset. Stay diversified, check hidden costs, and focus on long-term consistency instead of short-term wins.

8. Can I invest in U.S. ETFs from Europe?

Not directly. EU regulations under PRIIPs prevent retail investors from buying U.S.-domiciled ETFs. Instead, choose UCITS ETFs, which are European equivalents designed for transparency and investor protection.

9. How can I invest sustainably in Europe?

Look for ESG (Environmental, Social, Governance) or SFDR-compliant funds. Many brokers now offer ESG UCITS ETFs that track sustainability-focused indexes like MSCI Europe ESG Leaders or S&P Global Clean Energy.

10. What’s the best long-term investment strategy for small investors?

Stay consistent with ETF savings plans (Sparpläne), reinvest dividends, and add small amounts monthly. Over time, the combination of compounding and discipline will do more for your wealth than market timing ever could.

Iva Buće is a Master of Economics specializing in digital marketing and logistics. She combines analytical thinking with creativity to make financial and investment topics accessible to a broader audience. At Finorum, she focuses on translating complex economic concepts into clear, practical insights for everyday readers and investors.

Sources & References

Investment guides & beginner resources

EU regulations & taxation

- European Commission / Taxation & Customs — ESMA

- ESMA Retail Investor Report (2025)

- European Banking Authority (EBA)

- European Long-Term Investment Funds

- EU Taxonomy

- income protection

- Investor Compensation Schemes

- MiFID II (Markets in Financial Instruments Directive)

- paying off debt

- social safety nets

- Sustainable Finance Disclosure Regulation (SFDR)

- €1,200 and €2,000 per month

- Investopedia.com — dividend taxes vary

- KPMG EU Tax Centre

- PwC Tax Summaries

- Rue.ee — capital gains and dividends are taxable

- Wealthify.com — tax wrapper

Additional educational resources

- Amf-france.org — PEA

- Bafin.de — BaFin

- Bundesfinanzministerium.de — Freistellungsauftrag

- Centralbank.ie — Irish-domiciled UCITS fund

- Cnmv.es — CNMV

- Finanztip.de — ETF savings plans (Sparpläne)

- Gov.uk — ISAs

- Guinnessgi.com — Acc vs. Dist share classes

- Investopedia.com — compounding

- crypto.

- currency risk

- diversification

- essential insurance

- Investopedia

- Investopedia (2025)

- reframing spending money

- three months of expenses saved

- justETF — crowdfunding

- diversified mini-portfolio

- ETFs

- Morningstar (2025)

- Morningstar — low-cost UCITS ETF

- Oecd.org — OECD research on financial literacy