The situation with US ETFs in Europe often surprises new investors — the funds are popular and well known, yet still out of reach because of how EU rules are written.

Disclaimer:

The information provided on Finorum is for educational and informational purposes only and does not constitute financial, investment, or tax advice.

Investing involves risk, including the potential loss of capital.

Always conduct your own research or consult a qualified financial advisor before making investment decisions.

Finorum does not promote or endorse any specific financial products or institutions.

Introduction

For years, U.S.-domiciled ETFs such as SPDR S&P 500 (SPY), Vanguard S&P 500 (VOO), or iShares Core S&P 500 (IVV) looked unbeatable. Ultra-low fees, huge liquidity pools, straightforward exposures — most global investors treated them as the obvious benchmark. Almost the default option.

And here’s the twist.

From 2018 onward, European retail investors began hitting the same wall across multiple brokers. They opened Interactive Brokers, DEGIRO, Trading 212… searched for SPY or VOO… and the system simply refused the trade. No technical glitch. No missing quote. Just a blunt regulatory stop sign.

Why would a globally recognised ETF suddenly be off-limits in Europe?

The explanation sits inside PRIIPs, the EU’s framework for Packaged Retail and Insurance-based Investment Products. It’s not exactly intuitive at first glance — and that’s where most people start to get confused.

Under PRIIPs, every investment product offered to EU retail clients must publish a Key Information Document (KID). Three pages, tightly standardised, with risks, fees, and performance scenarios laid out in a very specific way. UCITS ETFs in Europe comply because they have to. U.S. ETF providers don’t, simply because U.S. law doesn’t require KIDs and the issuers have no regulatory obligation to create them for European retail investors.

And once that piece clicks into place, the rest becomes straightforward.

Without a KID, brokers are legally barred from offering U.S.-domiciled ETFs to retail investors in the EU. That’s why SPY, VOO, QQQ and similar funds appear purchasable on paper — yet remain inaccessible in practice. Even the largest brokers can’t override this.

So today, US ETFs in Europe have become largely inaccessible for the typical retail investor. UCITS ETFs stepped into that gap, not because they’re inherently superior, but because they satisfy the documentation requirements that U.S. funds do not.

If you want to see which UCITS funds European investors actually use instead of blocked U.S. tickers like VOO, SPY, or QQQ, start with

Best UCITS ETFs in Europe (2026)

What follows is a clear breakdown of why U.S. ETFs are restricted, how PRIIPs and UCITS shape this entire landscape, and which practical alternatives long-term European investors actually have. Not the theory — the day-to-day reality.

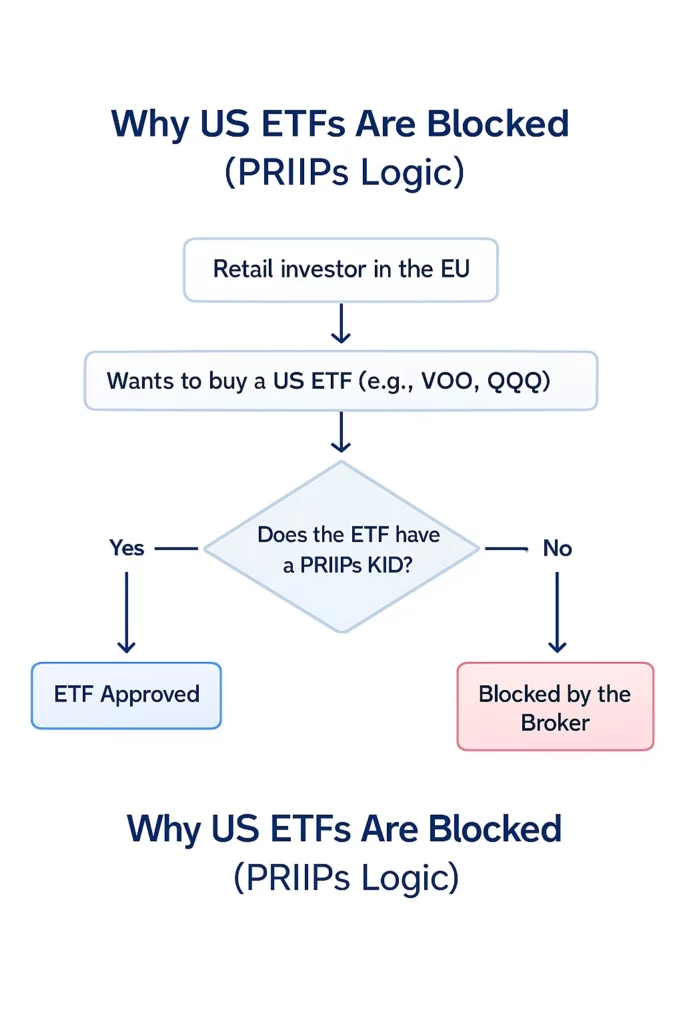

Why can’t Europeans buy US ETFs?

European retail investors generally cannot buy US-domiciled ETFs because these funds do not provide the PRIIPs Key Information Document (KID) required by EU rules. Without this document, brokers cannot legally offer them to retail clients in Europe.

PRIIPs Regulation Explained for European Investors

The PRIIPs regulation — Packaged Retail and Insurance-based Investment Products — has been quietly reshaping the European investment landscape since January 2018. Together with MiFID II and MiFIR, it forms the core of the EU’s investor-protection framework. MiFID II governs how products are sold and how advice must be delivered. PRIIPs determines what information retail investors must receive before they invest. Two systems, one shared goal.

But PRIIPs is where the real friction with U.S. ETFs begins.

Every eligible retail investment product in the EU needs a Key Information Document (KID) — a tightly standardised, three-page sheet that follows an identical structure across all issuers. No improvisation allowed. The KID must disclose:

- a concise description of the product’s objectives and features

- a detailed list of costs (TER, transaction costs, incidental fees)

- a risk score on a 1–7 scale

- several performance scenarios simulating different market conditions

Straightforward on the surface, but technically demanding behind the scenes. Producing a compliant KID requires financial modelling, legal input, and continuous updates. And that is the key reason U.S. ETF issuers like Vanguard or iShares US do not produce PRIIPs-compliant KIDs. They are not required to under U.S. regulation, and creating EU-specific disclosures for a foreign retail market simply doesn’t pass a cost–benefit test.

Here’s something many investors still overlook.

PRIIPs does not apply only to ETFs — it extends to a wide range of packaged products across Europe. The contrast becomes clear once you look at different product categories side by side:

| Product Type | PRIIPs KID Requirement |

|---|---|

| UCITS ETFs (Europe) | Mandatory KID |

| US-domiciled ETFs | No KID → not available to EU retail |

| Structured Notes | Mandatory KID |

| Insurance-based Investments | Mandatory KID |

| Specialized Funds | Mandatory KID |

This is the regulatory bottom line: no KID means no access.

Brokers across the EU are legally required to block retail clients from purchasing products that lack a compliant KID. It’s not a platform preference or a technical limitation — it’s a regulatory obligation.

If you want to understand how this restriction shapes real portfolio choices for everyday investors in the EU, read

Global vs European ETFs: Which Offers Better Returns for EU Investors?

For European retail investors, the implication is simple but important. If a product does not offer a KID, you will not be able to buy it, even if it is widely traded and perfectly accessible elsewhere in the world. And if the product looks complex or difficult to understand, speaking with a licensed financial advisor remains the safest approach. PRIIPs standardises the disclosures — it doesn’t guarantee that every product is suitable for every investor.

If a US-domiciled ETF doesn’t have a PRIIPs-compliant KID, the broker is required to block the order – regardless of how popular or liquid the fund is.

Why US ETFs Do Not Comply With PRIIPs Rules in Europe (2026)

At first glance, it seems odd. U.S.-domiciled ETFs like SPY, VOO, and IVV are among the most liquid and cost-efficient funds in global markets. Yet European retail investors cannot buy them. Not because the products are flawed — but because the disclosure rules in Europe do not match the regulatory framework in the United States.

And once you follow the regulatory trail, the logic becomes unavoidable.

Consider Nora, a retail investor in Finland. She can see SPY in her broker’s search bar. She can track its price. But when she tries to place an order, the system blocks the trade every single time. No technical error. No missing market data. Just the consequence of missing documentation.

Everything revolves around one requirement: the Key Information Document (KID).

1. No Legal Obligation in the United States

ETF providers in the U.S. operate under SEC rules. Those rules do not require a PRIIPs KID, nor anything similar. For U.S. issuers, Europe is not their primary retail market, and building a separate disclosure infrastructure for a foreign regulatory system is difficult to justify.

And here’s the part people often overlook:

U.S. providers aren’t refusing out of stubbornness — they simply have no regulatory reason to comply.

2. High Compliance Costs

A KID looks like a simple three-page PDF. It really isn’t.

Behind those three pages sits an entire compliance machine:

- legal reviews tailored to EU regulations

- financial modelling to generate standardised performance scenarios

- risk scoring using EU formulas

- mandatory updates whenever any underlying assumption changes

For a giant like Vanguard or BlackRock, this would mean maintaining hundreds of documents that serve no purpose in their domestic market. The cost–benefit calculation is straightforward — and the answer has been the same for years.

Most investors never realise how heavy that operational burden is.

3. Different Regulatory Frameworks

Structural differences deepen the gap.

U.S. ETFs follow ’40 Act fund rules.

European ETFs follow UCITS.

The two frameworks use different risk metrics, performance methodologies, and reporting formats. For US ETFs, translating their data into a PRIIPs-compliant form isn’t a simple template conversion. It requires reworking the structure of disclosures from the ground up.

Again: no obligation → no alignment → no KID.

4. Retail vs Professional Investor Access

Here’s a nuance that often causes confusion.

Professional investors — as defined under MiFID II — can buy U.S.-domiciled ETFs. They are exempt from PRIIPs requirements. Institutions, wealth managers, and certain HNW clients continue using SPY, QQQ, and similar funds without interruption.

Retail investors cannot.

Which is why brokers across Europe (IBKR, DEGIRO, Trading 212) actively block retail clients from placing orders in U.S. ETFs. It’s compliance, not choice.

Nora eventually realised this: she wasn’t doing anything wrong — the product simply lacked the document her broker is legally required to check.

Broader Implications for Investors

• Possible future reforms:

The European Commission periodically reviews PRIIPs. Some experts argue the rules misrepresent risk, others claim they oversimplify performance scenarios. Changes are possible — but timelines are uncertain.

• Why the KID matters:

A KID forces all products into one comparable format: costs, scenarios, risks. That’s the real idea — reduce surprises for ordinary investors who don’t read 150-page prospectuses.

• Impact on diversification:

The restriction limits access to the deepest and cheapest equity markets in the world. For some investors, especially those seeking ultra-low-cost broad exposure, it’s a noticeable constraint.

• Practical direction:

For now, UCITS ETFs are the default option in Europe. They are designed for the EU regulatory and tax environment and remain fully accessible. When complexity appears, a licensed financial advisor remains a sensible checkpoint. PRIIPs standardises information — it does not replace judgment.

And most people don’t realise how wide this gap is until they try placing their first order.

UCITS ETFs vs US ETFs under PRIIPs (Europe 2026)

| Feature | UCITS ETFs (Europe) | US ETFs (Domiciled in US) |

|---|---|---|

| PRIIPs KID Document | Provided (mandatory) | Not provided |

| Retail Investor Access (EU) | Available | Blocked by brokers |

| Professional Investor Access | Available | Available |

| Regulatory Framework | UCITS Directive + PRIIPs | SEC ’40 Act rules |

| Compliance Costs | Integrated into fund structure | Would require additional resources |

| Portfolio Use in EU | Primary option for retail investors | Restricted to professionals |

| Dividend Tax Impact | Typically ~15% at fund level (IE/LU) | 30% default; 15% with DTT + W-8BEN |

Reminder: If an ETF lacks a PRIIPs-compliant KID, your broker is legally required to block the order.

Impact of PRIIPs on European Retail Investors (2026)

The PRIIPs regulation has reshaped how European retail investors build portfolios — more than many expected back in 2018. Before PRIIPs came into force, buying U.S.-domiciled ETFs like SPY or VOO was routine. It was normal for Europeans to mix UCITS and U.S. funds side by side, benefiting from ultra-low fees and deep liquidity.

That world changed quickly once the KID requirement arrived — and the ripple effects are still visible in 2026.

1. Broker Restrictions

Every major European broker — Interactive Brokers, DEGIRO, Trade Republic, Trading 212 — enforces the same rule:

no PRIIPs KID → no access to US ETFs in Europe.

Anna, a retail investor from Germany, learned this the usual way. She entered an order for Vanguard S&P 500 (VOO). Everything looked fine until the final confirmation — and then the order was blocked. Her broker suggested UCITS alternatives such as:

Most investors don’t expect a regulation to reshape their portfolio in real time — but PRIIPs does exactly that.

And the first rejection usually comes as a surprise.

If you want to compare these UCITS alternatives against the European benchmarks many investors eventually choose instead, see

S&P 500 UCITS vs Euro Stoxx 50: A Comparison for 2026

2. Limited Choice and Higher Costs

Using UCITS ETFs instead of U.S. ETFs introduces two practical differences:

• reduced product variety

• slightly higher total expense ratios (TERs)

In the U.S., an S&P 500 ETF can cost 0.03%.

UCITS equivalents typically range from 0.07% to 0.15%.

It feels negligible.

Until you run the math.

On a €50,000 portfolio over 20 years at 7% annual growth, the gap between 0.03% and 0.15% quietly removes more than €2,000 from total returns. It’s not dramatic — but it’s real.

Case Study: Anna’s Portfolio Dilemma

Anna planned to invest €50,000 into VOO. When the order failed due to PRIIPs, she bought VUSA, the UCITS equivalent with a 0.07% TER.

Over 20 years at 7% growth, that TER difference cost her roughly €2,000 in potential gains.

Still, VUSA provided her with compliant exposure to the same index in EUR — avoiding FX conversions and aligning with European rules. Not ideal, but practical.

And this is the kind of trade-off most retail investors only notice after doing the numbers.

3. Currency and Tax Considerations

Many UCITS ETFs are denominated in EUR or GBP, which simplifies long-term planning for European investors. Fewer conversion steps, fewer hidden FX costs.

But UCITS funds also apply a 15% withholding tax at the fund level on U.S. dividends — a detail that often goes unnoticed. With U.S. ETFs, investors can usually file a W-8BEN to reduce withholding tax individually. With UCITS, the fund absorbs the tax internally and passes through the after-tax dividend.

It feels counterintuitive at first — but it’s simply how the EU–US tax treaties interact with fund structures.

Investor Reminder:

UCITS ETFs domiciled in Ireland or Luxembourg benefit from favourable tax treaties with the U.S., typically applying only 15% withholding. Always verify the domicile.

4. Portfolio Diversification Challenges

PRIIPs also narrows the universe of accessible products.

The U.S. ETF market is enormous — niche exposures, smart-beta strategies, thematic funds, ultra-cheap sector ETFs. Europe covers the essentials, not the full spectrum.

Theo in Greece described it well:

“The issue isn’t that UCITS are bad. It’s that the U.S. market offers everything — and Europe offers enough.”

For most retail investors, “enough” is fine.

For some strategies, it isn’t.

Retail vs Professional Access under PRIIPs (2026)

| Investor Type | Access to US ETFs | Access to UCITS ETFs |

|---|---|---|

| Retail Investor (EU) | Blocked — no PRIIPs KID | Fully available |

| Professional Investor | Allowed — PRIIPs exemption | Fully available |

Two investor categories, two completely different sets of possibilities.

Practical Notes for Investors

• Regulatory outlook:

The European Commission is reviewing the PRIIPs framework. Revisions may simplify disclosures or broaden access to U.S. ETFs in Europe — but timelines remain uncertain.

• UCITS “clones”:

Asset managers now offer UCITS ETFs designed to replicate popular U.S.-domiciled products like VOO, IVV, or QQQ. The exposure is similar; the structure differs.

• Cost awareness:

A small TER difference compounds significantly over time. Always compare fees when evaluating UCITS vs US ETFs alternatives.

• Professional advice:

Given the complexity around taxation and regulation, a licensed advisor remains a useful sounding board when uncertainty appears.

Investor Note

If your broker blocks a U.S. ETF such as VOO or QQQ, look for a UCITS equivalent:

- VUSA ≈ VOO

- CSP1 ≈ IVV

- EQQQ ≈ QQQ

These funds track the same markets — without violating the PRIIPs regulation.

UCITS ETFs: The Primary Alternative for European Investors (2026 Update)

With US ETFs in Europe effectively blocked for retail clients, UCITS ETFs have become the backbone of long-term investing across the EU. Their rise wasn’t about preference — it was about regulation. But over time, UCITS evolved from a workaround into a fully developed investment ecosystem: transparent, diversified, tightly regulated, and available on every major European exchange.

And the shift has been more profound than many investors initially realised.

1. PRIIPs Compliance and Accessibility

UCITS ETFs are fully PRIIPs-compliant, meaning they provide the required Key Information Document (KID). That single document unlocks retail access across Europe. Brokers, banks, robo-advisors — everyone can distribute them.

Take Anna again. Her VOO order failed, but Vanguard S&P 500 UCITS (VUSA) was only one click away. Same index. Same exposure. EUR-denominated and fully compliant.

Most EU investors end up navigating the UCITS vs US ETFs divide without ever thinking about it — until a blocked order forces the comparison.

If you want to see how European investors turn these UCITS substitutes into a simple, workable starter allocation, read

How to Build a €1000 ETF Portfolio in Europe

2. Costs and TER Differences

Let’s address the part investors always ask first: the fees.

- UCITS S&P 500 ETFs (CSP1, VUSA): 0.07%–0.15% TER

- US equivalents (SPY, VOO, IVV): 0.03% TER

UCITS are more expensive — but they are also accessible, tax-optimised for EU investors, and designed to sit comfortably inside the European regulatory system. For most retail investors, that convenience outweighs the fee gap.

The difference feels tiny, but compounding is persistent. Over 20 years, that extra 0.10% TER quietly eats into returns.

Case Study: Marco’s Global Portfolio

Marco from Italy wanted global exposure with no regulatory friction.

His three-fund UCITS portfolio:

- CSP1 → U.S. equities

- XMME → emerging markets

- VEUR → developed Europe

EUR-denominated, low cost, fully PRIIPs-compliant.

He never even needed to search for a U.S. ticker.

And here’s a detail many overlook:

tracking difference on major UCITS ETFs has tightened in recent years, often coming surprisingly close to U.S. counterparts — despite the TER gap.

3. Range and “Clone” Products

ETF issuers quickly adapted to the PRIIPs regulation by launching UCITS ETFs that mirror their U.S. equivalents. These “clones” track the same index and follow the same strategy — only the legal structure differs.

Examples:

- VUSA ≈ VOO

- CSP1 ≈ IVV

- EQQQ ≈ QQQ

For most investors, the experience is virtually identical.

4. Tax Efficiency and Currency Options

UCITS ETFs are typically domiciled in Ireland or Luxembourg, two jurisdictions with favourable tax treaties with the United States. This means:

- 15% withholding tax at the fund level (baked into the structure)

- no need for retail investors to file W-8BEN forms

- better tax treatment than the default 30% U.S. withholding on US-domiciled ETFs

Share classes also come in EUR, GBP, and USD, hedged and unhedged.

This gives European investors flexibility that U.S. ETFs simply do not offer.

And honestly, most investors underestimate how much currency swings shape long-term results — especially when savings plans run for decades.

5. Currency Risk and Thematic Growth

Currency fluctuations between EUR, GBP, and USD can materially distort returns.

Because of this, many UCITS ETFs now offer EUR-hedged and GBP-hedged variants, making long-term planning smoother.

Another trend has been impossible to ignore:

thematic and active UCITS ETFs are booming.

Investors now have access to strategies targeting:

- AI & semiconductors

- clean energy and climate solutions

- cybersecurity

- healthcare innovation

- next-gen infrastructure

- actively managed equity and bond funds

Europe’s ETF market is no longer “lagging” — it’s expanding.

6. Market Growth and Popularity

The UCITS ETF market surpassed $2.74 trillion (≈€2.5–€2.6T) in assets under management by mid-2025 — its highest level ever.

This momentum isn’t accidental.

It reflects a simple reality:

UCITS ETFs became the default vehicle for European investors seeking diversified, compliant global exposure without battling regulatory barriers.

Their growth mirrors investor behaviour: practical, regulation-aware, long-term focused.

UCITS vs US ETFs at a Glance (2026)

| Feature | UCITS ETFs (Europe) | US ETFs (Domiciled in US) |

|---|---|---|

| PRIIPs KID Document | Provided | Not provided |

| Retail Investor Access | Available | Blocked in EU |

| Typical TER (S&P 500) | 0.07% – 0.15% | 0.03% |

| Dividend Tax Treatment | 15% at fund level (Ireland) | 30% US withholding (15% with treaty) |

| Currency Options | EUR, GBP, USD (hedged/unhedged) | USD only |

| Fund Variety | Broad, rapidly expanding thematic/active | Largest & deepest ETF market |

PRIIPs Regulation: Criticism and Market Implications

The PRIIPs regulation was introduced to strengthen investor protection through clearer, standardised disclosures. A sensible objective. But the lived experience in the market has been more complicated. And here’s the strange twist — a rule designed to simplify choices has ended up restricting them.

Over the years, regulators, industry groups, brokers, and investors have all highlighted the same friction points. Some criticisms are technical; others are simply the reality felt on the ground. All of them shape how US ETFs in Europe are effectively blocked today.

1. Reduced Investor Choice

This remains the most visible — and arguably the most painful — consequence.

When PRIIPs became mandatory in 2018, thousands of U.S.-domiciled ETFs vanished from European broker platforms almost immediately. justETF captured the shift: a universe of liquidity, competition, and innovation simply became inaccessible to EU retail investors.

For Petra in the Czech Republic, the change was jarring.

She used to build her portfolio with a mix of U.S. and UCITS ETFs. Overnight, half her watchlist stopped being tradable.

The ripple effects are clear:

- fewer niche exposures

- fewer smart-beta options

- fewer ultra-low-fee funds

- fewer specialised bond and sector strategies

UCITS is solid — but it doesn’t match the breadth of the U.S. market.

Was this really the intended outcome? Many investors doubt it.

2. Questionable Value of KID Documents

The Key Information Document (KID) is the centrepiece of PRIIPs. But its real-world usefulness remains a subject of debate.

Industry bodies like EFAMA and Eurofi have argued that KIDs:

- oversimplify risk

- rely on rigid formulas

- and sometimes show performance projections that look almost too tidy

Several regulators even admit the issue quietly: the uniformity is helpful, but the prescribed scenarios can give investors a false sense of certainty.

Petra mentioned this after reading a KID for the first time:

“The chart looked optimistic — until I realised it was based on a formula, not the real world.”

A document meant to clarify risk can, oddly enough, soften it.

3. Higher Costs and Market Fragmentation

PRIIPs also increases costs in ways that aren’t always visible at first glance.

Because U.S. ETFs can’t be offered to retail investors, UCITS ETFs become the default substitute — even when they have:

- slightly higher TERs

- less variety

- narrower strategy coverage

Competition narrows. Costs rise subtly.

Case Study: Broker Costs Under PRIIPs

One mid-sized European broker reported that PRIIPs compliance added over €1 million per year in legal verification, IT integration, and scenario-modelling systems.

These aren’t abstract costs.

They feed into:

- higher trading fees

- reduced product menus

- slower rollout of new features

A regulation designed to protect investors ends up increasing the long-term cost of investing for many of them.

Irony? Absolutely.

4. Innovation Gaps

The U.S. ETF market continues to outpace Europe in:

- thematic strategies

- smart-beta innovation

- actively managed ETFs

- sector depth

- fixed-income variety

Europe is improving — the thematic UCITS boom in 2024–2026 is real — but PRIIPs effectively shields the EU market from U.S. competition. And without competitive pressure, innovation tends to slow.

UCITS is catching up, yes.

But the structural gap remains obvious to anyone comparing both markets side by side.

5. Ongoing Regulatory Debate

PRIIPs may be established law, but it’s far from settled policy.

Within the European Parliament, ESMA, and policy groups like Eurofi, the conversation is active. Critics argue that the regulation needs substantial refinement:

- more realistic scenarios

- disclosures based on actual risk drivers, not formulas

- better alignment with MiFID II

- potential exemptions for large, liquid U.S. ETFs

The PRIIPs Review 2025 is already underway, and expectations for changes are growing — though no one agrees on what the final outcome should look like.

Broader Regulatory and Market Challenges

The debate extends well beyond ETFs:

• Protection vs competitiveness:

Too much protection can make Europe structurally less attractive than the U.S. or Asia — a recurring theme in industry reports.

• Industry feedback:

Asset managers and brokers report increased operational complexity, reduced product innovation, and higher compliance overhead (EFAMA).

• Future regulation:

The Commission is reconsidering how KIDs are structured — aiming for clearer, more realistic, less formula-driven information.

• Fragmentation and liquidity:

PRIIPs contributed to a marketplace where ETFs may only list on certain exchanges, reducing cross-border efficiency. ESMA continues to push for better integration.

In practice, the EU is trying to walk a tightrope: protect investors without suffocating market dynamism.

Pros and Cons of PRIIPs Regulation (2026)

| Aspect | Intended Benefit | Criticism / Market Impact |

|---|---|---|

| Investor Protection | Simplified disclosures (KIDs) | KIDs can be misleading or overly optimistic |

| Market Transparency | Standardised information | Excludes US ETFs → reduced competition |

| Cost Impact | Clear cost breakdowns | Higher TERs + added compliance costs |

| Investor Choice | Easier comparability | Fewer options, slower innovation |

| Market Liquidity | Greater retail safeguards | Fragmentation + reduced cross-border efficiency |

Tax Differences Between UCITS and US ETFs for European Investors (2026 Update)

Taxes rarely feel urgent at the start — until they quietly reshape your returns over decades. And for European investors choosing between UCITS vs US ETFs, taxation is where the biggest real-world differences emerge. Regulation may block access to U.S. funds, but tax rules determine how much performance you actually keep.

What surprises most investors is how similar — and yet subtly different — the outcomes can be.

1. Withholding Tax on Dividends: The Core Issue

The most important tax detail comes down to how dividends are treated.

US-domiciled ETFs

- Default U.S. withholding tax: 30%

- Reduced to 15% with W-8BEN

- But… PRIIPs blocks EU retail investors from buying these ETFs in the first place

UCITS ETFs (Ireland & Luxembourg)

- Flat 15% withholding at fund level, applied automatically

- No forms to file

- No access issues

The key takeaway:

For U.S. equity exposure, UCITS and U.S. ETFs usually end up paying the same 15% withholding tax.

Many investors still assume U.S. ETFs are “more tax-efficient”, but that gap closed years ago — especially after PRIIPs.

2. Fund Domicile Matters More Than People Think

Ireland and Luxembourg dominate because both benefit from favourable U.S. tax treaties.

- Irish UCITS → 15% withholding

- Luxembourg UCITS → typically 15%

- Other domiciles → sometimes higher withholding

So the real question isn’t just “UCITS or U.S.?”

It’s: “Where is the UCITS ETF domiciled?”

Nora from Finland discovered this when she compared two nearly identical S&P 500 UCITS ETFs — their tracking difference diverged purely due to domicile-driven tax mechanics.

If you want a broader look at how tax structure, domicile, and index selection come together in practice, see

Best European Index Funds (2026)

3. Capital Gains Treatment: The Quiet Equaliser

Another common misconception:

“A U.S. ETF gives better capital gains tax treatment.”

For Europeans — it doesn’t.

Capital gains are taxed according to your country of residence, regardless of ETF domicile.

So whether you buy UCITS or (hypothetically) a U.S. ETF, your tax treatment is shaped by:

- Germany → Abgeltungsteuer

- Italy → 26% capital gains tax

- France → PFU flat tax

- Netherlands → Box 3 wealth tax

- Spain → progressive savings tax

The tax battleground is dividends, not capital gains.

4. Accumulating vs Distributing UCITS ETFs

This is an area where UCITS gives Europeans more flexibility.

UCITS ETFs come in:

- Distributing classes (payouts)

- Accumulating classes (reinvest dividends internally)

In some European systems (Germany, Belgium, Austria), accumulating share classes reduce or delay taxable events. In others, synthetic taxation rules equalise the outcome.

But the core benefit remains:

UCITS gives you a choice. U.S. ETFs don’t.

5. Tracking Difference: The Hidden Tax Cost

Even when ETFs track the same index, tax mechanics and internal operations affect real performance.

Tracking difference (TD) reflects:

- dividend withholding

- securities lending revenue

- replication method

- management style

- reinvestment timing

Interestingly, many UCITS ETFs have improved their tracking difference over the last five years — sometimes outperforming their stated TER through securities lending income.

Luca from Italy noticed this firsthand.

Comparing CSP1 and VOO over a five-year window, he expected a massive gap. Instead, the difference was surprisingly small — most of it driven by FX movements, not tax.

An important reminder: TER rarely tells the full story.

Some UCITS ETFs use synthetic replication, especially in niche or hard-to-access markets. Tax implications here can differ slightly, but for major indices like S&P 500 or MSCI World, the effect is usually modest.

6. FX Exposure and Share Class Options

U.S.-domiciled ETFs are USD-only.

UCITS ETFs offer:

- EUR

- GBP

- USD

- hedged and unhedged classes

For long-term savers, avoiding constant FX conversions can itself become a tax-efficient strategy — especially for monthly or quarterly investment plans.

And honestly, many investors underestimate how much currency volatility shapes results over 15–20 years. It’s often the biggest unseen performance factor.

UCITS vs US ETFs: Tax Comparison (2026)

| Tax Aspect | UCITS ETFs (Ireland/Luxembourg) | US ETFs (Domiciled in US) |

|---|---|---|

| Dividend Withholding Tax | 15% at fund level (automatic) | 30% default → 15% with W-8BEN (if allowed) |

| Capital Gains Tax | Based on investor’s country | Based on investor’s country |

| FX Exposure | EUR/GBP/USD options, hedged classes | USD only |

| Dividend Handling | Distributing & accumulating share classes | Distributing only |

| PRIIPs Retail Access | Fully available | Blocked for EU retail (no KID) |

Common Mistakes European Investors Make Under PRIIPs (2026)

PRIIPs didn’t just change the product landscape — it changed the behaviour of European investors. And because these rules aren’t always intuitive, people still fall into the same traps again and again. Some mistakes are harmless. Others quietly cost thousands over long horizons.

Here are the most common ones — and why they matter more than many expect.

1. Assuming US ETFs Are Still Accessible to Retail Investors

Even in 2026, many first-time investors still try buying SPY, VOO, or QQQ, only to hit the same brick wall:

no PRIIPs-compliant KID → order blocked.

Theo from Greece once messaged his broker thinking it was a technical error. It wasn’t.

It was simply regulation doing what it’s designed to do.

The mistake isn’t trying — it’s planning a portfolio around funds you can’t legally buy.

2. Ignoring the Impact of Fund Domicile

Many investors compare UCITS ETFs purely on TER — and stop there.

But domicile (Ireland vs Luxembourg vs other jurisdictions) can materially influence:

- withholding tax

- tracking difference

- reinvestment mechanics

- overall performance

Nora discovered this when two S&P 500 UCITS ETFs with identical TERs delivered noticeably different returns. The culprit wasn’t fees — it was the tax treaty behind the domicile.

3. Confusing Performance Scenarios in the KID

The KID document is meant to clarify risks, but its performance scenarios often puzzle new investors.

They can look:

- optimistic

- formula-driven

- disconnected from real-world volatility

And that’s because they often are.

A common mistake is trusting KID projections as if they were forecasts.

They’re not.

They’re regulatory templates, nothing more.

Luca once joked that KID “made every ETF look like a savings account.” He wasn’t entirely wrong.

4. Focusing Only on TER and Ignoring Tracking Difference

This is one of the most expensive mistakes.

Investors look at TER because it’s simple.

But tracking difference (TD) is the real outcome — and it’s influenced by:

- dividend withholding tax

- securities lending revenue

- replication method

- internal timing

- FX

- fund efficiency

A UCITS ETF with a 0.07% TER can outperform one with a 0.05% TER if it has better tracking mechanics.

Investors who focus only on the expense ratio often miss this.

5. Underestimating Currency Exposure

Currency swings can distort long-term returns far more than a 0.10% TER gap — yet many investors barely think about FX.

Euro-based savers buying USD-only funds often face:

- conversion costs

- performance distortion from USD/EUR cycles

- higher volatility

- tax complexities in some jurisdictions

UCITS hedged classes exist for a reason.

But many investors only consider them after several years of unpredictable FX-driven fluctuations.

6. Assuming US ETFs Are Always More Tax-Efficient

This used to be true — pre-PRIIPs.

But today, UCITS ETFs domiciled in Ireland or Luxembourg often achieve comparable, sometimes even better, after-tax outcomes due to:

- favourable US tax treaties

- internal fund-level withholding optimisation

- accumulating share classes

- lower FX friction

Many investors cling to outdated assumptions from forum posts dating back a decade.

The landscape changed.

7. Forgetting That Accessibility Is a Feature

One of the most overlooked mistakes is assuming the “best” ETF is the one with the lowest TER or deepest liquidity — even if it can’t be held, taxed, or reported easily in Europe.

A fund you can’t buy is academically interesting, but practically irrelevant.

A fund you can buy, hold, tax-declare, and automate monthly…

That’s the real benchmark.

Marco understood this when he stopped chasing U.S. tickers and built a clean, compliant UCITS portfolio he could actually maintain.

8. Ignoring the Long-Term Impact of PRIIPs on Costs

Few retail investors connect the dots between:

- regulatory complexity

- broker compliance burdens

- reduced product menus

- narrower competition

- slightly higher TERs

Yet all of this quietly compounds over decades.

PRIIPs shapes the market more than most investors realise.

Long-Term Outlook: Will Europe Ever Regain Access to US ETFs? (2026 Perspective)

The question keeps resurfacing:

“Will European investors ever regain access to U.S.-domiciled ETFs?”

It’s a fair question — and a complicated one. PRIIPs has been in place for eight years, and while the rule is widely criticised, it hasn’t collapsed under pressure. But the regulatory landscape is shifting again, and there are signs (some subtle, some explicit) that change is at least being discussed.

Here’s the long-term outlook as it stands.

1. EU Policymakers Know PRIIPs Has Problems — That Matters

Within the European Commission, ESMA, and the Parliament’s ECON committee, the tone has changed.

Not dramatically, but noticeably.

Several issues have been acknowledged:

- performance scenarios in KIDs are flawed

- retail access to global markets is narrower than intended

- PRIIPs indirectly raises costs

- disclosures, in their current form, sometimes confuse instead of clarify

- fragmentation makes the EU less competitive vs. the U.S.

This doesn’t guarantee reform — but acknowledgment is the first prerequisite for change.

2. The PRIIPs Review 2025 Could Be a Turning Point

The ongoing PRIIPs Review 2025 is the most significant opportunity for structural revision since the regulation was introduced.

Three scenarios are being debated behind the scenes:

Scenario A: Modify KID rules

Make performance scenarios more realistic and allow alternative disclosure formats.

Impact on U.S. ETFs:

Possible, but indirect.

Scenario B: Create a “light” KID for large, liquid ETFs

This is the mildest version of reform.

Impact on U.S. ETFs:

Potentially opens the door for selected U.S. funds.

Scenario C: Exempt widely used U.S. ETFs

This is what investors want — but policymakers hesitate.

Impact:

Would instantly allow SPY, VOO, QQQ, IVV, etc. back into EU retail accounts.

Political likelihood: modest but not impossible.

The industry prefers Scenario C. Regulators lean toward Scenario A.

That tension will define the next 2–3 years.

3. Would U.S. Issuers Even Care Enough to Create EU-Compliant KIDs?

This is the part many investors underestimate.

Even if the EU changes the rules, U.S. issuers must still want to comply.

Vanguard, BlackRock (US), and State Street would need to:

- generate KIDs

- update them regularly

- maintain EU-specific risk models

- coordinate with European regulators

Would they do it?

Possibly — but only if demand and cost-benefit align.

Right now, the EU retail market is attractive, but not essential.

4. UCITS Ecosystem Is Getting Stronger Every Year

There’s another reality:

Europe no longer “needs” U.S. ETFs as much as it did pre-2018.

By mid-2025:

- UCITS AUM passed $2.74 trillion

- tracking differences tightened

- more thematic ETFs launched

- active UCITS ETFs expanded

- hedged share classes became mainstream

In other words:

Europe built its own ETF machinery.

That reduces pressure to re-open the U.S. market.

If regulators look at UCITS and say, “This works well enough,”

change becomes less urgent.

5. The Political Layer: Investor Protection vs Global Competitiveness

The EU always balances two priorities:

- protect retail investors, and

- remain competitive on global capital markets

If PRIIPs is seen as undermining competitiveness (and many policymakers now say it is), reforms become more likely.

If political momentum shifts toward stricter protection after a market shock, reforms could stall for years.

This is why predicting timelines is nearly impossible — it’s not just economics, it’s politics.

6. The Most Realistic Long-Term Outcome

Based on trends across 2024–2026:

Most likely scenario:

A modified KID framework allowing simpler disclosures, but still requiring documentation from issuers.

→ UCITS remains dominant.

→ Some U.S. ETFs may regain limited retail access if issuers participate.

Medium likelihood:

A targeted exemption for a small set of major, highly liquid U.S. ETFs (S&P 500, Nasdaq-100, Total Market).

→ Would immediately open up VOO, IVV, QQQ.

→ Politically sensitive, but not impossible.

Low likelihood:

A full reversal where all U.S. ETFs become accessible again.

→ This would require philosophical change at the EU level.

→ Currently unlikely.

So, will Europe regain access to U.S. ETFs?

Eventually — yes, but partially.

Not a full reopening. Not anytime soon.

More likely: a slow, incremental opening driven by disclosure reform.

The shape of that reform will depend on how the EU balances investor protection with its ambition to compete with U.S. capital markets.

Until then, UCITS ETFs remain the long-term core of European retail investing — not because they’re perfect, but because the system has grown around them.

Conclusion: The Reality of US ETFs in Europe (2026)

PRIIPs wasn’t designed to block U.S.-domiciled ETFs — but that’s exactly what it did. Eight years later, Europe lives with the consequences: reduced access to the deepest ETF market in the world, higher compliance burdens, and a retail ecosystem built around UCITS by necessity, not preference.

What’s interesting is how the market adapted.

UCITS ETFs didn’t just fill the gap — they grew into a full-scale investment infrastructure, with better tracking, broader themes, smarter replication, and AUM that rivals global peers. The system is far from perfect, but it works, and most European investors now build entire portfolios without ever touching a U.S. ticker.

Still, the core truth remains.

This isn’t a product debate — it’s regulatory architecture. And unless the EU rewrites parts of the PRIIPs framework, retail investors won’t be placing orders for VOO or QQQ anytime soon. The long-term direction is clearer than the timeline: some reform is likely, full access is not.

In practice, UCITS will continue to anchor European portfolios — not because they are always better, but because they are the only structure that fits inside the rules.

If you’re starting from scratch and want the clearest path into investing under European rules — without wasting time on products you can’t legally buy — begin with

How to Invest €1000 in Europe (2026 Guide)

Key Takeaways

PRIIPs blocks U.S. ETFs for retail investors — not brokers.

If a fund has no KID, the order must be rejected. Platforms aren’t choosing to block access; they’re following the law.

UCITS ETFs became Europe’s default because they fit the regulatory system.

They’re PRIIPs-compliant, tradable on every major exchange, and structurally built for European investors.

The tax gap between UCITS and U.S. ETFs is smaller than people think.

For U.S. equities, both structures typically lose the same 15% dividend withholding—just through different mechanisms.

Focusing only on TER is a mistake.

Tracking difference, domicile, replication, reinvestment timing and FX have a far bigger impact on real returns.

UCITS offers practical advantages that U.S. ETFs simply don’t.

Accumulating share classes, EUR-denominated units, and hedged variants make portfolio management easier for Europeans.

KID documents remain controversial.

They simplify comparison but can misrepresent risk through rigid, optimistic scenarios.

Innovation still runs faster in the U.S., but Europe is narrowing the gap.

Thematic and active UCITS ETFs have expanded rapidly since 2024.

Regulatory reform is likely, but full reopening is not.

Expect adjustments to disclosures or limited exemptions—not a return to pre-2018 access.

Many investor mistakes come from outdated assumptions.

What was true before PRIIPs no longer applies today.

For most Europeans, UCITS ETFs remain the most practical long-term option.

Not because they’re perfect, but because they work seamlessly within EU tax and regulatory rules.

FAQ: US ETFs, PRIIPs & UCITS Explained (2026)

Because these ETFs don’t provide a PRIIPs-compliant Key Information Document (KID). Without a KID, EU brokers are legally required to block retail access. It’s a regulatory issue, not a platform preference.

Not for retail clients. Only MiFID II–defined professional investors can buy U.S. ETFs directly. Retail investors must use UCITS alternatives.

Not necessarily. For U.S. equity exposure, UCITS funds domiciled in Ireland or Luxembourg typically pay the same 15% withholding tax as U.S. ETFs with a W-8BEN. The tax gap people remember from pre-2018 is largely gone.

Yes. Most UCITS ETFs mirror their U.S. equivalents almost exactly — for example, VUSA ≈ VOO, CSP1 ≈ IVV, EQQQ ≈ QQQ. The difference is the regulatory wrapper, not the index.

Slightly higher TERs and fewer niche strategies. For broad market exposure, the difference is small; for thematic or smart-beta strategies, the U.S. often still offers more variety.

Because they’re generated using rigid formulas that can produce overly optimistic projections in rising markets. They describe scenarios, not forecasts — and that distinction is often misunderstood.

In some countries, yes. Accumulating share classes defer or reduce taxable events; in others, tax rules neutralise the benefit. The impact depends entirely on your local tax system.

Tracking difference. TER is the list price; TD is the actual outcome after taxes, replication costs and reinvestment timing. For many indices, UCITS ETFs with higher TERs still outperform lower-cost rivals.

Possibly, but not fully. The most realistic outcome is a revised KID framework or limited exemptions for large, liquid U.S. ETFs. A complete return to pre-2018 access is unlikely.

Yes. UCITS ETFs offer global diversification, solid tracking, accumulating classes, hedged options, and efficient tax treatment for Europeans. They’re not perfect — but they fit European rules better than any alternative.

Matias Buće has a formal background in administrative law and more than ten years of experience studying global markets, forex trading, and personal finance. His legal training shapes his approach to investing — with a focus on regulation, structure, and risk management. At Finorum, he writes about a broad range of financial topics, from European ETFs to practical personal finance strategies for everyday investors.

Sources & References

EU regulations & taxation

- Betterfinance.eu — performance scenarios

- European Commission / Taxation & Customs — Key Information Document (KID)

- MiFID II and MiFIR

- PRIIPs

- PRIIPs

- Oecd.org — EU–US tax treaties

- White-label.hanetf.com — UCITS ETFs domiciled in Ireland or Luxembourg benefit from favourable tax treaties

Broker comparisons & investing platforms

Additional educational resources

- Assetservicingtimes.com — Industry bodies like EFAMA and Eurofi have argued that KIDs

- Efama.org — thematic and active UCITS ETFs are booming

- UCITS ETF market

- Fidelity.com — Tracking difference (TD)

- Investopedia.com — financial modelling

- Investor.vanguard.com — Vanguard S&P 500 (VOO)

- Irs.gov — W-8BEN

- Ishares.com — iShares Core S&P 500 (IVV)

- justETF — In the U.S., an S&P 500 ETF can cost 0.03%

- iShares Core S&P 500 UCITS (CSP1)

- UCITS ETFs

- US ETFs in Europe have become largely inaccessible

- Vanguard S&P 500 UCITS (VUSA)

- Law.com — legal input

- Msci.com — Most UCITS ETFs mirror their U.S. equivalents almost exactly

- Sec.gov — 40 Act fund rules

- Ssga.com — U.S.-domiciled ETFs such as SPDR S&P 500 (SPY)